Ethics in FX advertising: FinanceFeeds investigates why warehouse brokers are allowed to advertise as STP

Small brokerages with warehouse execution models and high leverage are continuing to advertise their services using the acronyms ‘STP’ and ‘ECN’, alluding to their processing of orders directly to live markets via aggregated liquidity via prime of primes and non-bank communication networks. We investigate why this occurs

Ever since the evolution of retail FX which has taken it from its original format in which the MetaTrader 4 platform provided a closed environment for firms to only operate via their own dealing desks and create their own market into today’s environment in which retail FX brokerages can emulate the institutional sector by providing live pricing and direct access to aggregated interbank currency markets, there has been one particular area which still requires some development in order to achieve complete transparency.

That area is the means by which smaller retail brokers present themselves to their customers via advertising and how they describe their services.

Three letter acronyms such as STP (Straight Through Processing), DMA (Direct Market Access) and ECN (Electronic Communications Network) are often used without explanations of their meanings in order to describe the execution method offered by many small firms that do not have access to such systems.

Straight Through Processing refers to the methodology in which FX brokerages do not internalize trades within their own dealing desk, instead sending them to their liquidity provider and taking no internal risk whatsoever. Of course, depending on who provides their services, the liquidity provider, especially if it is another retail brokerage, is then at will to internalize the orders that have been sent by the retail broker claiming to execute orders on a Straight Through Processing basis, meaning that to tell customers that orders are processed in this manner is misleading.

Despite this, many small, often newly established firms come to market with an advertisement to their customers stating that they offer STP execution, when it is, given the extreme difficulties in obtaining credit from Tier 1 banks in the interbank FX liquidity provision business these days, very unlikely to be the case.

Just five years ago, it was possible to establish a relationship with a Prime of Prime with approximately $5 million, but today, the banks are demanding between $25 million and $50 million for a prime of prime relationship, meaning that smaller firms are priced out completely and only well capitalized businesses with established capital bases and high levels of assets are able to gain access to a direct market via a prime of prime these days without taking some of the risk themselves.

Of course, in some cases, smaller brokers may be able to gain a price feed from a prime brokerage and then use that price feed to execute according to the prices from the liquidity provider in house, thus creating an emulation of a live market without the risk or having to have the counterparty relationships in place, and this is perfectly legitimate, but still does not constitute STP execution.

There is a litany of such material listed on several websites of small warehouse brokerages, some of which make absolutely impossible claims toward sending their orders directly to the liquidity provider.

Ordinarily, Australia’s financial markets regulatory authority ASIC is one of the most astute in the world when it comes to ensuring that brokerages making implausible claims are prevented from doing so, often resulting in removals of licenses and winding up of companies. Indeed, ASIC has presented its concern in its bi-annual reports several times over the last few years stating that its priority is to prevent margin FX firms with less than ethical modus operandi from doing business, resulting in Australia’s worldwide respected business environment which is, in terms of FX industry participants, among the very best in the world.

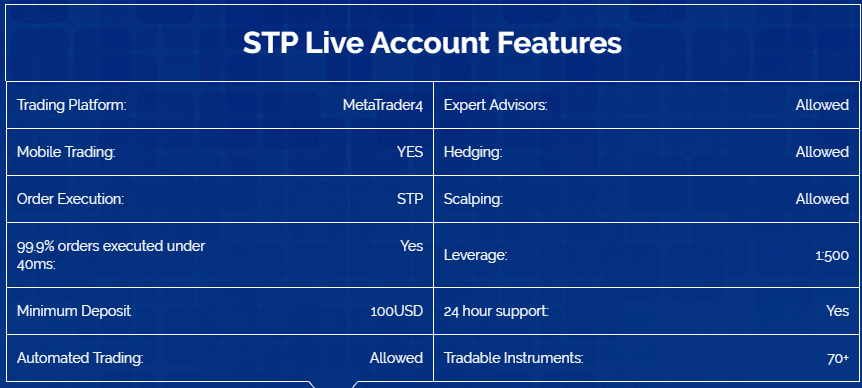

Still, there is the occasional exception. SynergyFX, licensed by ASIC, makes this claim on its website:

Making a claim to offer leverage to retail customers at a ratio of 1:500 even if execution is taking place on a b-book basis is alarming enough, as most of the time, small retail accounts will not be capitalized enough in the live market to be able to make any winning trades, and in ALL recognized regulatory jurisdictions, offering such high leverage to retail clients is illegal, except for with dealing desk licenses in Cyprus.

Aside from the regulatory disdain for high leverage around the world, and the odds which are stacked against retail customers in such a highly leveraged environment, there is absolutely no way possible that any retail firm would be able to execute trades via a liquidity provider rather than their own dealing desk at this ratio.

The extension of credit, and risk management procedure of Tier 1 banks to OTC derivatives firms is at an all time low. Banks absolutely do not want to extend credit, even to firms that operate in recognized jurisdictions, are massively well capitalized and have a maximum leverage ratio of 1:25.

Citibank, the world’s largest interbank FX dealer by percentage of global order flow (over 16% of the global Tier 1 FX liquidity market) has stated that it considers the extension of credit to OTC derivatives firms and liquidity providers a potential default risk ratio of an astonishing 56% – and that is among top quality and well capitalized business which is conducted in top quality regions. Not small firms offering 1:1500 under any circumstances.

Putting out a message to potential customers that they are able to execute trades at a ratio of 1:500 on a live market is, in our opinion, completely misleading, and is damaging to our otherwise very sophisticated industry whose top quality companies in Britain, Australia, Cyprus, North America and the Far East are continually striving for the provision of the best quality trading environments for their customers.

Further examples of claims to offer Straight Through Processing have become increasingly prevalent. Under CySec regulations, a broker which has a license to operate as a market maker and warehouse trades via its own dealing desk must have a provision within their license that is clearly marked “Dealing on Own Account”, which is listed as one of the provisions.

A license to be a market maker requires a minimum capital adequacy requirement of 730,000 Euros, whereas a license to process all trades directly to the liquidity provider only requires 125,000 of net capital, therefore several firms display that they are not dealing on own account, however the most important aspect to bear in mind here is that whilst they are likely not internalizing trades on their own dealing desk, often they do so at the desk of a sister company, an offshore entity, or another retail brokerage whose dealing desk provides the trading environment via a white label solution, internalizing it at the point that it reaches said dealing desk, thus direct relationships with Tier 1 bank aggregated liquidity via a prime of prime are not in place, or the ability to process trades directly via non-bank ECNs such as Currenex, Hotspot FX, EBS or FXall is also not present.

Many examples of the prominent advertising of such services exist today. Traders Trust, which is also known as TTCM, which acquired the clients of LCG CEO Charles-Henri Sabet’s JFX Capital Markets two years ago, makes a clear statement on its website that it offers direct market access.

As per the aforementioned example, Traders Trust also states that it provides 1:500 leverage on an STP basis:

PriorFX has a similar advertising campaign, in which the company claims to offer straight through processing on this basis. FinanceFeeds contacted the company for a statement as to why this is being promoted in public areas, however no comment was proferred.

FinanceFeeds approached CySec in order to ask why retail brokerages with a warehouse execution model that executes trades internally or sends orders to another warehouse broker that they take their services from are allowed to advertise in this manner, especially on home territory.

CySec did not provide a comment with regard to how this is allowed, however, the spokesman for the regulator to which we highlighted this matter explained to FinanceFeeds that he has passed this onto senior officials.

FinanceFeeds understands that it is unlikely that any regulator globally would provide comment on a specific company on or off the record, but understands that as a result of our research, CySec will be bringing this to the attention of the surveillance department in order that they can investigate fully.

Brokerages in the FX industry go to great lengths and vast expense in order to provide top quality direct market execution to their customers, ensuring that they abide by the regulatory rulings, provide massive capital adequacy in order to cover trades with the liquidity provider and to ensure the constant negotiations for trade processing are accurately carried out with prime brokerages and ultimately Tier 1 banks, therefore the ability to quantify themselves as brokers that have STP execution should be preserved and not diluted by warehouse brokerages that claim to be on the same level as those whose corporate structure is top quality.

FinanceFeeds maintains that there is absolutely nothing wrong whatsoever with operating an internal dealing desk, and in order to minimize risk to clients which could experience exposure to negative balances due to market volatility, to increase the speed of execution during highly active periods during the trading day or to be able to operate a smaller brokerage and not have to lodge vast capital sums with the prime brokerage, this is fine as long as the orders are being executed in accordance with the correct prices from a live pricing feed. In short, b-book execution, if done according to a live price feed, is absolutely fine in terms of business practice, but claiming to offer STP execution and direct market access when it is clear that this is not the case, is a different matter altogether.

Thus, highlighting this to regulatory authorities and to other industry participants is as important as the transparency between quality broker and client.