Kraken, the second-largest U.S.-based cryptocurrency exchange, has acquired the cryptocurrency arm of online brokerage TradeStation.

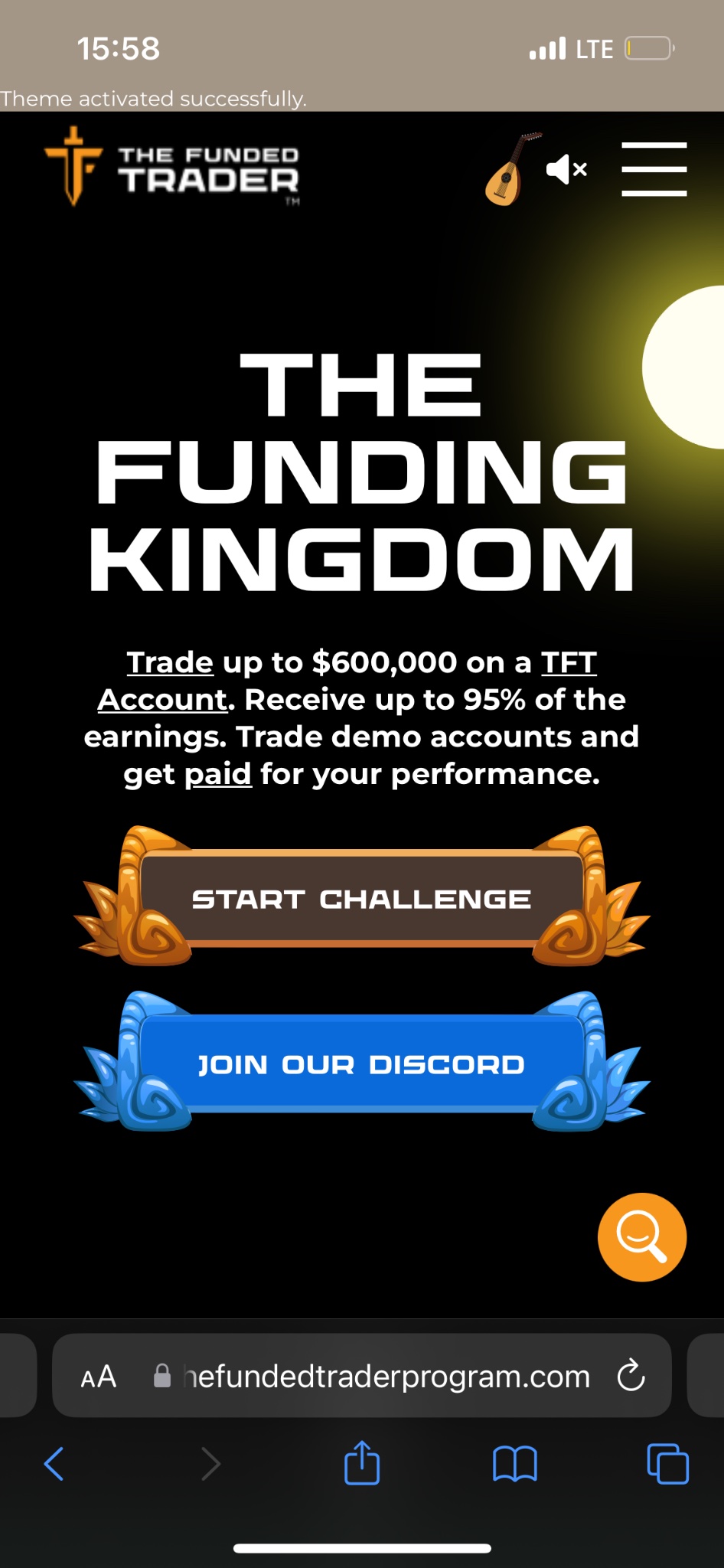

Prop trading firm The Funded Trader has updated its website with a few banners, nearly three weeks after it ceased all operations, with claims for a relaunch in the near future. However, there was no official statement on the relaunch on its website, Discord channel, or social media accounts yet.

NAGA Group, a provider of brokerage services, cryptocurrency platform NAGAX and neo-banking app NAGA Pay, appointed Loukia Matsia as their new Head of Compliance and Anti-Money Laundering (AML).

Navigating the vast ocean of cryptocurrencies might feel overwhelming for many investors, whether seasoned or newbies.

EURUSD currency pair can be expected to fall further toward the next support level 1.0600 (which reversed the price earlier this month).

Binance, the world’s largest cryptocurrency exchange, has obtained a Virtual Asset Service Provider (VASP) license in Dubai.

“Their participation further strengthens our collective efforts to drive positive industry change and greater sustainability in the global markets trading industry.”

“With its unique combination of KYC-compliant identity verification, real-time fraud prevention solutions, and expert support, VideoIdent Flex is a powerful tool for the UK market.”

The mid-term plan will be to integrate DVS’s Guarantee Vault with D7, the digital post-trade platform of Deutsche Börse and its post-trade business Clearstream. This will allow D7 for the first time to expand its digital asset product portfolio to non-securities.

Prop trading firm The Funded Trader has updated its website with a few banners, nearly three weeks after it ceased all operations, with claims for a relaunch in the near future. However, there was no official statement on the relaunch on its website, Discord channel, or social media accounts yet.

Malaysia will be the first region to try out the new, improved version of OctaTrader, a customisable cross-device trading platform finely attuned to the needs of all traders regardless of their experience. To support the release of new OctaTrader features, Octa launches a global communication campaign The lucky ones, which will highlight some key aspects of the traders’ psychology and attitude to luck.

Interactive Brokers has expanded its suite of investment options for Japanese clients with the addition of CFDs on US stocks.

“The launch of ODP will strengthen HKEX’s capability to support the needs of global investors, and cement Hong Kong’s leading position as Asia’s risk management centre and an international financial centre.”

“StoneX Payments proudly services more than 80 bank customers across the US, EU, UK and APAC regions, including many of the world’s largest and systemically important banks, offering 140+ currencies across 180 countries.”

Trading software and liquidity services provider Finalto has gone live with its Over-the-counter Derivative Product (ODP) Liquidity Solution in South Africa in early 2023.

Interactive Brokers has expanded its suite of investment options for Japanese clients with the addition of CFDs on US stocks.

Recent developments in the currency markets depict contrasting trajectories for the US dollar (USD) and the British pound (GBP). While the USD continues its upward trend, bolstered by a series of positive performances, the GBP finds its footing amidst a backdrop of mixed economic indicators.

The US dollar continues its upward trajectory, buoyed by robust retail sales figures and shifting expectations around Federal Reserve rate cuts.

Coinbase International Exchange (CIE) will introduce perpetual futures trading for Solana-based memecoin dogwifhat ($WIF), starting April 25. These open-ended futures contracts can be traded using the USDC stablecoin.

Kraken, the second-largest U.S.-based cryptocurrency exchange, has acquired the cryptocurrency arm of online brokerage TradeStation.

Binance, the world’s largest cryptocurrency exchange, has obtained a Virtual Asset Service Provider (VASP) license in Dubai.

As the Bitcoin community counts down to the upcoming Bitcoin halving, Mark Zalan, CEO of GoMining, shared exclusive insights into how the company is gearing up for this pivotal event in the cryptocurrency world.

Celebrating its 14th anniversary, Tools for Brokers (TFB), hosted a private networking event in Cyprus, gathering industry professionals to discuss future trends and innovations.

For access to the full interview and to explore more about Finalto’s contributions to the FX industry, you can visit the March 2024 edition of e-Forex magazine.

Every four years, the crypto world gets hyped for the Bitcoin halving. Past halvings, like the one of May 2020, saw a massive increase in BTC transactions, which was driven by growing adoption and community involvement.

One of the most important events for every Bitcoin user and investor is upon us. The event known as halving plays a pivotal role in the Bitcoin system, and it will affect its value, as well as supply and demand.

DeFi lending is attractive as it offers much higher interest rates than the average bank savings account, but investors should also be aware that using these protocols can be much riskier than depositing money into a traditional financial institution.

Mon Protocol and Pixelverse make history in the annals of Blockchain gaming as they set up the architecture for the melding of their technologies.

FBS, a leading global broker, introduces its revamped mobile trading application – the FBS app. The upgraded solution is available for Android and iOS users, providing them with all the tools and resources for online trading.

Step into the new phase of digital realms with Somnia’s L1 blockchain and omnichain protocols, designed to link various virtual experiences and improve content creation.

Explore the innovative Megadrop platform on Binance, offering early access to new Web3 projects and a chance to earn unique rewards.

The report jointly presented by QuickNode and Artemis provides an in-depth analysis of the blockchain ecosystem’s evolution in the last quarter, particularly focusing on user activity, significant developments across different blockchain chains, and emerging trends in the web3 space.

Embark on the Future: Binance App Surges with 6.3M Downloads in 2024’s Dawn, Redefining Crypto Accessibility. Dive into the World of Web3 with Binance’s Intuitive Interface and Join Over 183M Users in the Financial Revolution. Trust, Security, and Limitless Possibilities Await.

NAGA Group, a provider of brokerage services, cryptocurrency platform NAGAX and neo-banking app NAGA Pay, appointed Loukia Matsia as their new Head of Compliance and Anti-Money Laundering (AML).

OKX, the world’s second-largest cryptocurrency exchange by trading volume, has seen the departure of two of its top executives, Tim Byun and Wei Lan, according to a report from CoinDesk.

Binance.US has appointed Martin Grant, a former chief compliance and ethics officer at the Federal Reserve Bank of New York, to its board of directors.

FV Bank now lets clients deposit euros directly into USD accounts, streamlining international business banking and offering a wider range of deposit options for its global clientele.

PayRetailers Arg S.R.L.’s recognition as a PSP Aggregator by the Central Bank of the Argentine Republic enhances its payment services in Argentina, emphasizing efficient and secure solutions.

In recent years, the integration of cryptocurrency payments within the realm of Forex trading has surged dramatically. This transition signifies a profound shift in the financial landscape, offering a wide range of benefits for both brokers and traders alike.