CFD regulation and the global impact – A comprehensive guide

James O’Neill, Director of ILQ Australia Pty Ltd, examines the differing regulatory requirements applying to contracts-for-difference across Australia, Cyprus, the UK and the US, makes a comparative study of OTC leveraged derivatives in selected jurisdictions, looking at rules relating to the handling of client money, fair market pricing and capital requirements.

James O’Neill is Director of ILQ Australia Pty, and is a qualified lawyer, with a Juris Doctor and Master of Laws degree from University of Sydney in Australia.

The research was developed by James O’Neill and published in full by TRAction Fintech on its website as a follow-on from the recent MiFID II seminars held in London and Limassol.

In my view, ASIC’s regulatory omission of rules dealing with fair market pricing is left wanting. Similarly, CySec’s rules on fair market pricing are also inadequate and are potentially damaging to CFD issuers if followed assiduously. CySec’s rules effectively prohibit negative slippage.

Over a prolonged period of time and in a market full of scalpers (clients whose trading strategy is to ‘hit’ brokers off-market) this could result in the bankruptcy of brokers. The author commends the NFA and FCA for their rules on fair market pricing. Though, different in their approach, both operate to ensure that brokers can operate within the general market while prohibiting nefarious behaviour when it comes to pricing of the financial instruments. – James O’Neill, Director, ILQ Australia Pty

As an introductory preamble to the research conducted here, it is important to look at the origins of the contract-for-difference, often referred to by the acronym CFD.

A CFD is an agreement under which you may make a profit or incur a loss from fluctuations in the price of the contract.

CFD providers will generally quote bid and offer prices at which the provider is willing to enter into long or short contracts with clients over an online platform.

Clients are generally required to fund their trading account (known as posting initial margin) which allows them to trade. Trades are made on a margined basis; this means that the amount which is required to place a trade does not match the notional value of the underlying asset and is typically in the range of 1%-50% of the notional value.

Industry practice dictates that this margin amount is quoted as a ratio, for example a 2% margin is quoted as 50:1.

The CFD is said to have been originally developed in the early 1990s by Messrs Brian Keelan and Jon Wood, while they were employed on the Smith New Court derivatives desk.

However, transactions similar in nature to CFDs can be found as early as the 19th Century. For example, Grizewood v Blane concerned an agreement where parties contemplated no delivery of equity securities but only settlement of difference in price. At Smith New Court, CFDs initially

represented a cost-effective way for hedge fund clients to short the London stock market, as they were able to take advantage of leverage and benefit from stamp duty exemptions.

Size of the Market

CFDs and specifically Margin FX comprise one of the largest segments of the world’s financial markets; foreign exchange markets transact 5.4 trillion US dollars every day. Due to the high degree of leverage within the specifications of these products, it is not uncommon for small to medium size firms offering CFDs to trade USD 1 billion (known as a “yard”) per day, with bigger operations trading multiples of this figure.

The International Organization of Securities Commissions (“IOSCO”) in its report into retail OTC leveraged products notes “the regulation in reporting jurisdictions is quite heterogenous” .

Australia

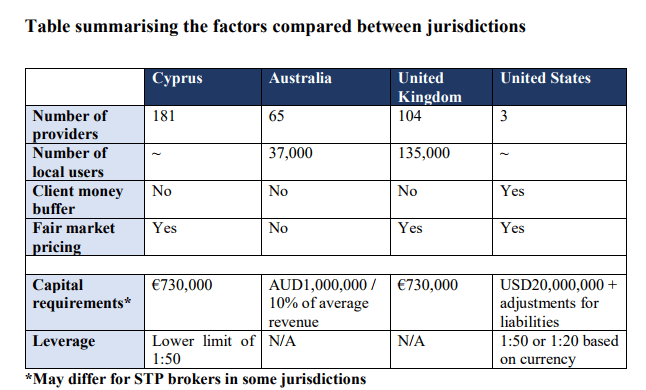

The CFD industry in Australia is in its infancy by comparison to the well-developed market in the UK. CFDs first appeared in Australia in March 2002 when CMC Markets entered the Australian market. IG Markets closely followed, entering Australia in July 2002. As of June 2016, there were 65 OTC derivative issuers.8 According to research firm Investment Trends there were approximately 37,000 active CFD traders in Australia in 2016, down from 49,000 active traders in 2015.

The Australian market is dominated by two providers, IG Markets and CMC Markets who combined, make up 56% of the market.

The Australian component of FX volume is sizeable and growing with total average daily volumes across over-the-counter (OTC) markets amounting to $134.8 billion in April 2016.

Companies wishing to offer CFDs must hold an Australian Financial Services (“AFS”) Licence, authorising them to advise, deal by issuing and make a market in derivatives (and foreign exchange contracts if the broker wishes to offer CFDs over currency pairs, known as Margin FX).

Cyprus

Cyprus is one of the most popular jurisdictions for CFD providers with 181 licensed CFD providers as of March 2017.

Online CFD Forum The FX View speculates that the primary reasons for CFD providers to set up in Cyprus are the favourable tax regime; European Union membership and light touch regulation, going so far as to comment: The regulatory requirements in many countries far exceeds the minimums as required by MiFID, however Cyprus has taken a relatively light touch approach to financial regulation.

This makes it much cheaper for brokerages to be regulated by CySec, than other European regulators such as Britain’s FCA or Germany’s BaFIN.

United Kingdom

The United Kingdom is seen as a mature CFD market. As at December 2016 there were 104 firms authorised by the Financial Conduct Authority (“FCA”) to provide CFDs, with an estimated 135,000 active users of CFDs.

United States of America

Regulation of CFDs in the United States is governed by the Commodity Exchange Act. Firms offering CFDs must be registered with the US Commodities and Futures Trading Commission (“CFTC”), as either a retail foreign exchange dealer (“RFED”) or a Futures Commission Merchant (“FCM”).

These firms must also be forex dealer members of the National Futures Association (“NFA”). According to IOSCO, there were 6 FCM/RFED firms. However, as at the date of writing there remain three firms who are RFEDs which offer CFDs, being GAIN Capital Group LLC; Interactive Brokers LLC and OANDA Corporation.

This is a significant decrease from 52 firms who acted as counterparties to retail forex clients in 2007 (together holding USD 1.3 billion in client funds). A further 181 firms existed acting as introducing brokers. The United States’ NFA crackdown on the industry has contributed to this reduction with large listed CFD provider FXCM the latest to relinquish its licence in early 2017.

Client Money

When it comes to regulating CFDs, one of the more critical aspects for the protection of investors is how client money is dealt with. Each jurisdiction has different rules for the treatment of client money, that is, how it needs to be held and accounted for, the manner in which client money may be used and importantly, when client money may not be used.

The importance of this was apparent in the case of In re MF Global Australia Ltd (in liq).

In that case, MF Global Australia used their ability to use client money to hedge to its parent company which on 31 October 2011 declared bankruptcy with an estimated US$1.6 billion of client funds being lost.23 From the clients’ perspective, laws surrounding whether money deposited is held on trust or not are important. In order for money to be held on trust, it must be segregated from company funds and therefore, is protected in the event of the CFD issuer’s insolvency.

Australia

In Australia, the treatment of client money is dealt with by Part 7.8 of the Corporations Act 2001 (Cth). Detailed analysis of the application of this to OTC derivative issuers is provided by ASIC in ‘Regulatory Guide 212: Client money relating to dealing in OTC derivatives’ (“RG 212”), which defines what client money is. RG 212 stipulates that client money is money paid to an AFS licensee:

(a) In connection with either a financial service that has been provided (or that will or may be provided to a client or a financial product held by a clients, and

(b) Either:

(i) By a client or a person acting on behalf of a client; or

(ii) to the licensee in the licensee’s capacity as a person acting on behalf of the client.

The client money provisions do not apply to:

(a) Money paid as remuneration to a licensee;

(b) Money paid to reimburse (or discharge a liability incurred by) the licensee for payment made

to acquire a financial product;

(c) Money paid to acquire a financial product from the licensee;

(d) Loan money; or

(e) Money paid to be credited to a deposit product.

Handling client money is governed by s 981 of the Corporations Act 2001 (Cth). Specifically, s 981B of the Corporations Act 2001 (Cth) requires that client money must be deposited into a designated client money account which is operated as a trust account.

This account must be segregated from company funds.

A licensee may make payments out of a client money account in the following circumstances:

(a) Making a payment to, or in accordance with the written direction of, a person entitled to

the money;

(b) Defraying brokerage and other proper charges;

(c) Paying to the licensee money to which the licensee is entitled; and making a payment that is otherwise authorised by law or pursuant to the operating rules of a licensed market.

Currently, section 981D applies in respect of dealing in derivatives. It provides the following:

Despite anything in regulations made for the purposes of 981C, if:

(a) The financial service referred to in subparagraph 981A(1)(a)(i) is or relates to a dealing in

a derivative; or

(b) The financial product referred to in subparagraph 981A(1)(a)(ii) is a derivative;

The money concerned any also be used for the purpose of meeting obligations incurred by the licensee in connection with margining, guaranteeing, securing, transferring, adjusting or settling dealings on behalf of people other than the client.

In simple terms, this provision allows CFD issuers to use client money for the purposes of hedging with another broker. This increases counterparty risk significantly. Client money which remains in the designated trust account will not be subject to creditors of the CFD issuer in the event that the CFD issuer becomes insolvent. Under s981D, the CFD issuer may place client money with a third party for the purpose of hedging.

To endeavour to remedy this issue, the Australian Government in October 2015 announced that it would develop legislation to better protect its root and branch examination of Australia’s financial system. On 1 December 2016 the Treasury Laws Amendment (2016 Measures No. 1) Bill 2016 was introduced into Federal Parliament, with the intention of, amongst other things, “removing the exemption in the client money regime that allows Australian financial service licensees to withdraw client money provided in relation to retail OTC derivatives from client money trust accounts, and use it for a wide range of purposes including working capital”.

The Bill passed both Houses on 27 March 2017 and received Royal Assent on 4 April 2017. In commenting on the changes to the client money rules, ASIC Commissioner Cathie Armour stated:

“The amendments to the client money regime made in the Bill have strengthened the protection of client money that is provided to retail derivative clients. Doing so will help to increase investor confidence in the Australian financial system.”

Market participants are less confident these amendments will provide the intended benefits and protections for investors. Financial services expert and solicitor, Sophie Gerber made the following observation in relation to the changes to client money rules:

This has been a very divisive issue in the industry. What may have been a more beneficial approach to this issue would be to have disallowed the use of the Corporations Act provisions for using client money for margining/hedging etc. with related parties and also prohibiting the payment of any forms of conflicted remuneration in these relationships. Time will show us whether these reforms have or have not benefitted the industry, I think unfortunately in this case the retail client will not see any benefits, and over the next few years the outcomes will be reduced competition and increased cost.

While these changes are an excellent step towards ensuring that client money is protected from credit risk from the issuer who may have significant exposure to the vagaries of the market, the changes do not provide full protection for retail clients. Their money is pooled with other clients’ money.

As a result, retail clients are still exposed to counterparty risk. This may occur where the OTC derivative issuer makes a withdrawal from a client money account of money that is entitled to be used under s981D. This could result in total client liabilities exceeding the amount in the client trust account. With insufficient funds remaining in the client trust account if the OTC derivative issuer becomes insolvent, the clients would receive less money than they are strictly entitled to – Sophie Gerber, Director, TRAction Fintech

Additionally, ASIC prohibits segregated trust accounts from including a buffer of house funds. In contrast, other jurisdictions require that there is excess money in the client trust account to ensure there is never a client shortfall.

Cyprus

The treatment of client money is specified in both the Investment Services and Activities and Regulated Markets Law of 2007 (“Regulated Markets Law”) and Part VI of CySec Directive DI144-2007-01 of 2012 (“Directive”). Section 18(2)(j) of the Regulated Markets Law states:

“A Cyprus Investment Firm (“CIF”) must, when holding funds belonging to clients, make adequate arrangements to safeguard the clients’ rights and, except in the case of credit institutions, prevent the use of client funds for its own account.”

“Under section 18(1)(e) of the Directive, CIFs must ensure that clients’ funds are held in accounts identified separately from company accounts. CIFs must conduct regular reconciliations of client accounts and company funds.31 CIFs are required to report information on clients’ funds to CySec on a quarterly basis with an annual audit submitted to CySec verifying these quarterly reports. ”

United Kingdom

The treatment of client money by derivative issuers is dictated by the Client Asset Sourcebook (“CASS”) which is published by the FCA. CASS 7.13 stipulates that “The segregation of client money from a firm’s own money is an important safeguard for its protection”. CASS restricts CFD issuers from depositing money which is not client money into the client trust account.

Furthermore, the FCA requires that all client money is directly deposited into the segregated client money account rather than to the CFD provider’s account and then further deposited into a segregated client trust account. An individual client’s money may be pooled with other clients’ money.

The FCA does not allow client funds to be used for hedging purposes.

Fair Market Pricing

As CFDs are derivatives traded over-the-counter, one issue that is prevalent within the market and should be a concern for all regulators is fair market pricing.

Fair market pricing refers to ensuring that the price on transaction is in-line with general market expectations. One issue that complicates this is a phenomenon known as slippage. Liquidity and frictional costs may also have an impact on the slippage percentage.

Fair market pricing is fundamental to a fair, honest and transparent financial services industry and allows participants to have confidence in the relevant financial market.

Regrettably, the nature of trading means that slippage is unavoidable. However, best practice dictates that on the law of averages slippage should be symmetrical. Slippage in the client’s favour indicates predatory trading and/or arbitrage on behalf of the client and if prevalent and repeated in perpetuity will lead to broker insolvency. Pricing in the broker’s favour indicates unethical trading practices on behalf of the broker.

Australia

Australia does not have any specific legislation mandating pricing of CFDs and slippage. The Australian financial services regulatory system does, however, provide a general obligation on all AFS licence holders to act efficiently, honestly and fairly.

There is yet to be any jurisprudence as to whether a AFS licensee’s general obligations would extend to ensuring that slippage is symmetrical. Caselaw confirms the meaning of efficiently, honestly and fairly, which must be read as a compendious indication meaning a person goes about their duties efficiently having regard to the dictates of honesty and fairness, honestly having regard to the dictates of efficiency and fairness, and fairly having regard to the dictates of efficiency and honesty.

Additionally, Enderby J’s comments in Nisic’s Case that ASIC “is entitled to rely upon and consider those part [industry conventions related to stockbroking] of the business of the plaintiffs in licensing matters”48 suggests that courts may be willing to read fair market pricing into the ambit of s 912A(1)(a) of the Corporations Act 2001 (Cth).

Justice Young provided obiter that s 912A(1)(a) “is obviously designed to protect the public”. Other examples within the Corporations Act 2001 (Cth) provide examples of prohibitions to mispricing such as Pt 7.10 Div. 2 which contains market manipulation, false trading, market rigging and false or misleading statements relating to financial products and services.

These themes are echoed by Mason J in North v Marra Developments to ensure that the market reflects the forces of genuine supply and demand. By supply and demand” I exclude buyers and sellers whose transactions are undertaken for the sole or primary purpose of setting or maintaining the market price.

It is in the interests of the community that the market for securities should be real and genuine, free from manipulation.

In the author’s view, it would be unlikely that a CFD issuer who engages in asymmetrical slippage will infringe on false trading, market manipulation, market rigging or false or misleading statements relating to financial service products. This is because of the definition of making a market in s 766D(1) of the Corporations Act 2001 (Cth):

A person makes a market for a financial product if:

(a) Either through a facility, at a place or otherwise, the person regularly states the prices at which they propose to acquire or dispose of financial products on their own behalf;

(b) Other persons have a reasonable expectation that they will be able to regularly effect transactions at the stated prices; and

(c) The actions of the person do not, or would not if they happened through a facility or at a place, constitute a financial market.

As the financial product is issued by the CFD provider, the CFD provider must state prices at which other persons have reasonable expectations that they will be able to regularly affect prices. Persistent positive slippage (that is, slippage in favour of the client) may result in fewer orders being filled and the CFD provider either increasing spreads or only partially filling orders. While there is a strong possibility that asymmetric slippage would infringe on the likelihood of the issue being tested by a court is remote.

For this reason it is the author’s view that legislative reform may be required to ensure fair market pricing. Financial Services expert, Sophie Gerber contributed her perspective on this matter:

Unlike the OTC derivative industry, market participants (e.g. on the ASX) in Australia have a best execution obligation (RG223) and for a retail client, a market participant must take reasonable steps when handling and executing an order to obtain the best outcome for the client.

It is possible that ASIC may impose similar obligations on the OTC derivative industry down the line, however this has not been mentioned as far as I’m aware. I believe this is primarily because ASIC doesn’t have sufficient expertise or resources for enforcing this type of provision.

ASIC may also impose relevant disclosure obligations on licensees regarding their execution practices to allow retail clients to make more informed decisions on whether to invest and who to invest with. – Sophie Gerber, Director, TRAction FinTech

Cyprus

Cyprus laws relating to fair market pricing come under the Investment Services and Activities and Regulated Markets Law of 2007. It provides that CFD issuers must:

1. Act honestly, fairly and professionally in accordance with the best interests of their clients and provide adequate information to clients about the financial instruments offered (Article 36).

2. Take all reasonable steps to obtain, when executing orders, the best possible result for its clients taking into account price, costs, speed, likelihood of execution and settlement, size, nature or any other consideration relevant to the execution of the order (Article 39).

3. Implement procedures and arrangements for the execution of orders that provide for the prompt, fair and expeditious execution of client orders (Article 38).

Readers will note that Article 36’s initial limbs exhibit a similar flavour to those drafted in Australia’s general obligations. The obligations in the Cyprus regulations go further than the Australian equivalent requiring firms to act in the best interests of their clients in addition to providing adequate information to clients about the financial instruments.

The pertinent issue here is whether disclosure of symmetrical slippage would discharge the CFD provider’s duty to act in accordance with the best interests of the client.

Article 38 appears to be a reasonable one, it requires firms to provide reasonable pricing when offering prices for orders looking at the general market conditions and the size and nature of the orders. For example, a client who is trying to execute a large trade, for example US$15 million, is likely to receive a larger spread than a client who is executing a small transaction.

In times of market volatility, spreads are generally going to be wider than low volatility periods and Article 38 seems to take this into consideration. Of benefit to clients, CySec on 13 February 2017 published some guidance into how they interpret Article 38 stating “CIFs must execute orders on terms most favourable to clients”.

United Kingdom

In the UK, fair market pricing is dealt with by the FCA within the Conduct Business section of the FCA Handbook.

CFD issuers have the following obligations:

11.2 Obligation to execute orders on terms most favourable to the client. A firm must take all reasonable steps to obtain, when executing orders, the best possible result for its clients taking into account execution factors. [Where execution factors is defined as price, costs, speed, likelihood of execution and settlement, size, nature or any consideration relevant to the execution of an order].

Application of best execution obligation

The obligation to take all reasonable steps to obtain the best possible result for its clients should apply to a firm which owes contractual or agency obligations to the client.

Dealing on own account with clients by a firm should be considered as the execution of client orders, and therefore subject to the requirements under MiFID, in particular, those obligations in relation to best execution.

If a firm provides a quote to a client and that quote would meet the firm’s obligations to take all reasonable steps to obtain the best possible result for its clients if the firm executed that quote at the time the quote was provided, the firm will meet those same obligations if it executes its quote after the client accepts it, provided that, taking into account the changing market conditions and the time elapsed between the offer and acceptance of the quote, the quote is not manifestly out of date.

The obligation to deliver the best possible result when executing client orders in relation to all types of financial instruments. However, given differences in market structures or the structure of financial instruments, it may be difficult to identify and apply uniform standard of and procedure for best execution that would be valid and effective for all classes of instrument.

Best execution obligations should therefore be applied in a manner that takes into account the different circumstances associated with the execution of orders related to particular types of financial instruments.

Requirement for order execution arrangements including an order execution policy A firm must establish and implement effective arrangements for complying with the obligation to take all reasonable steps to obtain the best possible result for its clients. In particular, the firm must establish and implement an order execution policy to allow it to obtain, for its client orders, the best possible result in accordance with that obligation.

The United Kingdom’s approach to fair market pricing is to require firms to obtain the best possible result for the client. The FCA rules do, however, acknowledge that market forces may not always result in zero slippage or positive slippage only. The rules add flexibility to allow negative slippage, however, there is a requirement that clients consent to an order execution policy. Firms that provide clients with asymmetrical pricing, not in the client’s favour, will contravene the legislation.

This provides clients with a reasonable amount of protection.

United States of America

In the US, the NFA has mandated the following with regards to fair market pricing:

Trading Platforms must be designed to provide bids and offers that are reasonably related to current prices and conditions.

Slippage.

An electronic trading platform should be designed to ensure that any slippage is based on real market conditions. For example, slippage should be less frequent in stable currencies than in volatile ones, and prices should move in clients’ favour as often as against them.

Additionally, the NFA also reads fair market pricing into its general requirement that no Forex Dealer Member or Associate of a Forex Dealer Member engaging in any forex transaction shall cheat, defraud or deceive, or attempt to cheat, defraud or deceive any other person; or engage in manipulative acts or practices regarding the price of any foreign currency or a forex transaction.

In its interpretative note on Rule 2-36, the NFA spoke about the application of the rule and cases involving infringing foreign dealer members:

The FDM used asymmetrical slippage settings that benefited the FDM to the detriment of the client because the slippage settings made it much more likely that a client order that moved against the client (and therefore the FDM’s favour) would be filled than one that moved in the client’s favour.

Any asymmetrical slippage settings or requoting practices or any other manipulative practices, that provide an advantage to the FDM to the detriment of the forex client would violate these rule provisions, including:

• The FDM set the maximum losing slippage (i.e., slippage that was unfavorable to the client and favorable to the FDM) at a much wider range of pips than the maximum profit slippage (i.e., slippage that was favorable to the client and unfavorable to the FDM). As a result, a client was much more likely to have an order filled when the market move was unfavorable to it than when the movement was favorable to the client.

• The FDM set the limit on the number of contracts in an order that could be executed that experienced losing slippage for the client at a much higher number than the limit on the number of contracts in an order that could be executed that experienced profitable slippage for the client. As a result, a larger sized order that moved against the client was much more likely to be executed than a smaller sized order that moved in the client’s favor.

• The FDM only passed negative slippage on to the client. If the FDM was able to offset the client’s order at a better price than the price at the time the client submitted its order, the FDM did not give the client the better price. However, if the FDM offset the client’s order at a price that had negative slippage and was unfavorable to the client, the FDM would thereby benefit from the slippage and fill the client’s order at the offset price.

The NFA’s approach makes it clear that slippage is likely to occur, and the CFD issuer is required to ensure that slippage occurs on a symmetrical basis and must not manipulate prices to ensure that pricing favours the broker.

Analysis

Pricing of derivatives is fundamental to transparency and confidence in the financial market, the financial product and the financial service provider. If the client believes that a product is skewed in the financial service provider’s favour, it erodes confidence. It is therefore imperative that jurisdictions that regulate CFDs ensure their laws deal appropriately with fair market pricing.

In the author’s view, ASIC’s regulatory omission of rules dealing with fair market pricing is left wanting. Similarly, CySec’s rules on fair market pricing are also inadequate and are potentially damaging to CFD issuers if followed assiduously. CySec’s rules effectively prohibit negative slippage.

Over a prolonged period of time and in a market full of scalpers (clients whose trading strategy is to ‘hit’ brokers off-market) this could result in the bankruptcy of brokers. The author commends the NFA and FCA for their rules on fair market pricing. Though, different in their approach, both operate to ensure that brokers can operate within the general market while prohibiting nefarious behaviour when it comes to pricing of the financial instruments.

With regard to capital adequacy requirements, in order to ensure that CFD issuers are reputable, a not insignificant barrier to entry is required.

Corporate regulators must also view capital adequacy as a mechanism against insolvency. The ASIC and CySec model does not in the author’s view meet a metric that the public should consider acceptable.

By design the capital requirements are static and may not incorporate the real-time exposure that the CFD issuer may require. For example, under the ASIC requirement the provider must have the greater of AUD 1 million or 10% of average revenue. It is quite possible that the provider on-boards a new client whose trades are significant from day one.

In the previous 12 months, the CFD issuer may not have had transactional flow that would require it to increase its capital requirement to a level that would be appropriate when taking into account the trades with the new client. Similarly, periods of losses may result in low revenues despite noteworthy trade flow.

The ASIC and CySec capital adequacy rules also do not mention volatility. The amount of capital required would need to be significant for the same notional value of transactions where volatility is high in comparison to a trading environment with low volatility.

One advantage of the CySec and ASIC model is its simplicity. It is easy to understand and therefore will be more likely to be complied with. In the author’s view the FCA model is the preferable model. The NFA’s USD20 million stymies competition and will mean investors are more likely to receive increased costs so that firms can operate with such a high capital requirement. The FCA model is not static and capital requires change as the firms receive more transactional flow (and risk).

Similarly, the FCA model recognises that some CFD providers do not take risk at all and they provide a lower capital requirement.