Chinese interbank FX liquidity rush is well on its way – Could this be future for Tier 1 bank PB?

A detailed examination of why London’s intebank FX Tier 1 bank dealers are waning, and where the liquidity is now centered. To those who think China cannot distribute its interbank liquidity outside, a second look is recommended !

East London’s Canary Wharf.

Home to the six global financial institutions that handle 49% of the entire world’s interbank FX order flow, and the central point that the entire global institutional and retail FX industry looks toward with regard to Tier 1 bank FX liquidity.

The glass towers that nestle along the once-desolate post-industrial docklands of Tower Hamlets may well sport names that betray their origins as German, North American, South African, Far Eastern and intrinsically British, however the entirety of the credible Tier 1 counterparties with their long-lauded single-dealer platforms being the final destination for most FX trades from brokerages across the world, are all completely London-centric in their operations.

The infrastructure that surrounds these banks is finely honed and is long-standing. Connectivity to global markets, data center hosting and the level of expertise within them unparalleled.

There is, of course, a giant elephant in the room, that being the constriction of counterparty credit that these dominant banks are willing to extend to the OTC derivatives sector, the very sector that for most of the large financial institutions, represents the vast majority of their core business revenue.

Whilst the retail banking divisions of the same banks flounder, expend tremendous resources on maintaining networks of physical branches, diversify into relatively low-value product ranges for financially stretched retail customers that then sue the banks for misselling, resulting in tremendous litigation costs and regulatory fines, lend small money overdrafts and unsecured credit to people with no intention or ability to repay, and handle small current accounts for provincial dependents who just scrape by each month, the electronic trading divisions of the same banks play their part in a $5 trillion per day FX market, from just one office.

Despite this evident advantage in efficiency from Western banks, they are wounded and jaded.

They are jaded from having experienced credit crunch after financial crisis, wounded from having too much presence in economically moribund and technogically outmoded European nations where no progress is made and operational costs are not worth the expenditure for the stagnant return.

They are reeling from regulatory fine after government censuring, and have been subject to publicly funded bailouts from the coffers of bankrupt socialist juggernauts such as the European Central Bank, which has as much knowledge of how the electronic markets operate as an alpaca does of operating a sewing machine.

Outside London, there is no electronic trading market to speak of in a continent of 500 million people.

London powers the entire continent from just one square mile which is evident in the output figures, those being that London’s entire financial sector employs just 0.0009% of the entire EU workforce, yet is responsible for 16% of all tax receipts.

Things are very different in the Far East.

Back in 1971, Toyota, a company that nobody had ever heard of, began importing cars to Britain. “Good grief, those Japanese are making cars!” quaffed the old school tie brigade from behind their cut-glass whiskey decanters, laughing it off from an aloof position of imperial decadence as though it was a bad joke.

It is not funny anymore, however.

Then the Korean companies and the Chinese began to do the same, and were met with the same derision as greeted Toyota’s Corona as the first one rolled off the Nippon Yusen Kaisha ships at Southampton docks.

That is also not funny anymore. In fact, the chances are that the very same individuals whose stiff upper lip curled and pointed with amusement at these “funny little things from the Orient” now take their daily trip to buy their (Chinese owned) Weetabix from Chinese-owned supermarkets in their Chinese or Korean-made car. What was that? Oh you drive a Volvo? That is also Chinese.

The Japanese, Korean and Chinese products arrived en masse, and very soon, it was recognized that whilst Britain’s workers were on the picket lines during James Callaghan’s Winter of Discontent and the refuse piled up in the streets and Derek Robinson’s destructive Shop Stewardship at British Leyland resulted in your vehicle not starting in the morning whilst your next door neighbor’s Datsun or Hyundai came to life immediately, and never missed a beat in its entire useful life.

The same is now happening to the creaking banks of London.

Citigroup issued a report last year starting that it expects a 56% default ratio to arise from the extension of counterparty credit to the OTC derivatives sector.

An alarming figure indeed. Hence, most other banks took heed and have restricted the extension of counterparty credit to prime of primes unless a balance sheet of between $50 million and $100 million can be displayed, and even then the answer may well be no.

There has been a massive reaction to this, and in many cases that have come to light over the past year, a plethora of companies have sprung up calling themselves Prime, when actually this is a triumph of marketing over substance because, especially given today’s grave credit situation, it is possible to count the actual number of prime of prime brokerages on one hand.

Among those that are genuinely Prime of Prime are Saxo Bank, Invast Global, Advanced Markets, Swissquote, CMC Markets, GAIN Capital GTX, ISPrime, Sucden Financial, CFH and AxiTrader.

CFH recently sold to Playtech, which may on the face of it appear to be a peculiar corporate decision, however given the choice of a capital injection (albeit of a FinanceFeeds estimate of a total of around $35 million, not the $120 million that was proposed – obvious when looking at the structure of the deal), would fend off a curtailing of credit by the bank’s prime brokerage division.

This morning, FinanceFeeds reported that Playtech considers its acquisition of CFH to be a demonstration of good performance and is looking at other M&As in this sector, which alludes to the same conclusion – that being that for those with smaller balance sheets but a good modus operandi, consolidation is inevitable.

Aside from this, there are very few other genuine prime of primes, and the difficulty to establish them for new firms is at its highest level.

Not so in China, or South Korea, however.

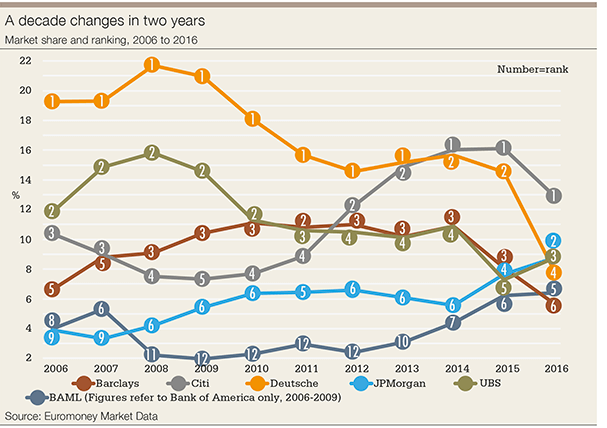

Take a look at the global market share, and the downward trend experienced by the major FX dealers of London, as per the Euromoney chart:

This is a contraction of global market share, yet in the West, they still dominate, so if that is the case, who is taking the remainder of the market share?

China, that is who.

In January, I stood in front of 400 senior Chinese FX industry executives and explained that within a very short time, China will dominate its own domestic market FX industry. Several years worth of extensive research by FinanceFeeds senior management inside China alongside strategic Chinese partners across the entire country has demonstrated that the same constraints do not exist in China as they do outside China.

All were in agreement.

Last year was most certainly a year in which the entire prime brokerage sector was subject to a massive amount of evolution in the Western world, largely due to the increasing demand from brokerages for the best possible execution and access to the most accurate pricing and trade processing environment, as well as the counteraction to this, which has manifested itself in the major Tier 1 banks having curtailed the extension of credit to OTC derivatives firms due to their extremely conservative approach to counterparty credit risk.

This has created a situation in which the main Tier 1 banks are now ultra-conservative and are still licking their wounds by selling off retail divisions in their entirety, and restricting how much risk they take on counterparty credit extension to retail brokerages.

Complexity due to lack of credit and massive capital requirements? No problem in China

Meanwhile, brokers which have to face these counterparties have to stump up massive capital bases to maintain relationships with them and still be subjected to last look order execution on single-dealer platforms and then have to strike up relationships with further non-bank electronic communications networks such as EBS, Currenex, Hotspot FX and FXall in order to attempt to provide a more comprehensive liquidity solution against the banks’ pulling the rug out from under everyone’s feet.

The same brokerages are battling with this whilst focusing on mainland China, and its own restrictions toward allowing any transaction over $50,000 (which is nothing because most brokers have an omnibus account or a prime brokerage agreement and have to send much higher figures than that each month to overseas banks of the brokers they work with) out of the country for the purposes of derivatives trading.

China’s own banks, all of which are owned by the state, are massively well capitalized and have a very clever model indeed.

They do not expose themselves to risk, and they have assets which consist of property, cash, investments in company stock and indices that are so enormous that it is hard to quantify.

These banks, unlike the weary western banks, will extend counterparty credit to FX brokerages in China without the blink of an eyelid over risk.

Western banks are already wounded enough and are restricting what they can see quite transparently. It would be futile for a Western prime broker with no presence in mainland China to go to a Western bank’s eFX desk and ask for a large prime brokerage deal because of a massive Chinese partner that has been onboarded.

There is no way for the bank to check how large and how well capitalized that firm is, as one is one side of the firewall, and the other is, well, the wrong side.

The answer would be no.

For Chinese banks, offering Chinese liquidity to Chinese prime of primes and then distributing aggregated feeds to Chinese FX brokerages, the sky is the limit and this single factor, when it unfolds and is in place on a widespread scale, will cause the Chinese FX industry to absolutely mushroom in volume and power.

Prime of primes that have presence in China, that are not Chinese by origin, including Sucden Financial (HK) Ltd, Advanced Markets (Shanghai) and Saxo Bank’s APAC division will be able to participate very freely in this because they will be considered Chinese entities as they have their entire infrastructure based in China and therefore inside the firewall and under the all-seeing eye of the Chinese government.

There is also now new evidence that the Chinese government’s domestic-market-orientation is never going to wane, however the country’s banks are powering the APAC economy’s other strong FX areas that are a sleeping giant, unnoticed by Western eyes.

How can the major FX tier 1 dealers in London such as Barclays, JP Morgan, Citi, Deutsche Bank and HSBC as listed in the chart above have such a lowering market share, yet still be favored.

This is because China is entering the global arena via the back door. Of course, domestic FX industry executives in China know that only RMB liquidity can be offered at good rates and good execution by Chinese banks, the rest is foreign, and anathema to the Communist government, however looking at South Korea’s FX order flow figures for the past three months tells the story exactly how it is.

The daily FX turnover by local and foreign banks in South Korea rose 11.9% in the first quarter from the previous quarter, and the daily FX turnover averaged $49.98 billion in the January to March period, compared to the previous quarter’s $44.66 billion, according to the Bank of Korea.

So what? Well, South Korea is becoming an area of opening to the world for China’s FX liquidity. South Korea and China launched a direct exchange market for their currencies in December 2014, meaning that Yuan can be exchanged directly and then traded in other currencies and against other currencies by local and foreign banks in South Korea.

This has now been taken up by many participants and the daily trading volume of FX spots reached $19.41 billion in the first quarter of this year up 11.8% from the previous quarter.

Thus, South Korea itself may not be the originator of Tier 1 liquidity per se, but it is one of the outposts for Chinese connection from banks to the outside world, and is eating into global market share whilst said banks are unburdened with the woes of Western stalwarts.

As last year drew to a close, Singapore continued to dominate as the largest FX center in Asia for Interbank dealership.

The average daily trading volume of Singapore’s FX market was US$517 billion in April 2016, up 35% from US$383 billion in April 2013. Singapore’s share of global FX volumes has grown to 7.9% in 2016, from 5.7% three years ago.

The expansion in Singapore’s FX market was chiefly driven by growth in G10 and Asian currencies such as the Yuan (78%3), JPY (67%3), GBP (60%3) and Korean Won (55%3). Foreign exchange swaps made up the largest traded foreign exchange product class in Singapore and accounted for 48%4 of all trades, followed by spot (24%4) and FX forwards.

This clearly shows that the Chinese Yuan is using Singaporean bank trading desks as an outlet on the live international market, and the high Korean Won (KRW) figure shown here is likely due to the Yuan-Won direct exchange facilties in Korea.

Bear in mind that many brokers in China are looking to become increasingly dominant and have the purchasing power and balance sheets to gain whatever they want as most have over $250 million in assets under management and in some cases dwarf the brokers that they refer business to, and the market structured in this way represents the future.

Of the prime of primes that are mentioned above, all of them have significant presence in China, with local offices, local hosting and the ability to serve a local Chinese audience of brokerages with Tier 1 liquidity from within the mainland, Chinese management and Chinese systems that are government friendly.

A very smart move, because those who do not have any Chinese presence will soon be joining the inhabitants of the Jurassic era.