Look out for a broad equity sell-off and higher market volatility if US election is contested, says Saxo Bank

Saxo Bank heralds securing equity risk and commodity portfolios post US election as major Q4 consideration

Saxo Bank has today published its Q4 2020 Quarterly Outlook for global markets, including trading ideas covering equities, FX, currencies, commodities, and bonds, as well as a range of central macro themes impacting client portfolios.

“We fear that the U.S. election is the biggest political risk we have seen in several decades, as the end of the economic cycle meets inequality, social unrest and a market feeding frenzy driven by the policy response to this deep economic crisis: zero interest rates, infinite government and central bank support. The massive official backstop, with guarantees for demand and jobs in a world of state capitalism, means that markets and individual freedoms have never been more under attack.” says Steen Jakobsen, Chief Economist and CIO at Saxo Bank.

“At Saxo Bank Group, we see three distinct paths and probabilities between now and Inauguration Day on January 20, 2021: a contested election (probability 40%); a clean sweep by Biden (probability 40%); a win by Trump (probability 20%).

“Our job is to define consensus vs. reality and here we feel that the market is not properly pricing in both the risks of a contested result – the biggest risk for the markets, whether as a result of the contest itself or Trump’s objections and attempts to cry foul – or a clean sweep by Biden. Since both are a risk, this means volatility could rise dramatically.

“Our main message is that the U.S. election will come with increased volatility and risk. Whoever wins will not change the US direction much in aggregate. Both would spend huge amounts of money, both would lean on the Fed for supporting easy financing conditions and neither of them would seek deep reform. So to a large extent, the two Presidential candidates are the diametric opposite of what the U.S. needs.”

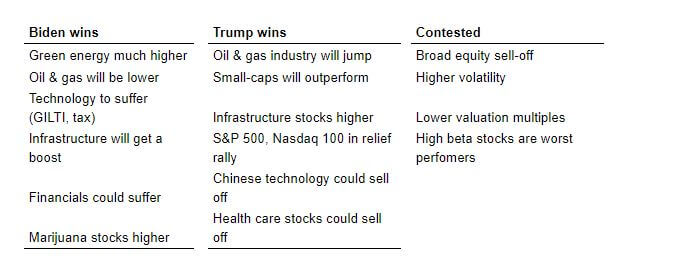

Structuring equity portfolios post-U.S. election

Supportive measures following the pandemic outbreak have engineered a strong rebound in equity markets and expectations are high going into Q3. The U.S. equity market has done quite well under a Trump administration and a Biden victory could bring added volatility and market drag in the form of increased taxes.

Peter Garnry, Head of Equity Strategy, said: “Aggressive policy action in the first half of the year by central banks and governments has engineered a strong rebound in equity markets and a general belief that the world will overcome the Covid crisis with less damage than from the 2008 financial crisis.”

“Expectations are high going into the third quarter earnings season, with estimates suggesting a 106% jump in quarterly earnings. If the corporate sector delivers this rebound in earnings, the global equity market will be valued at 19.3x earnings in 2021. Not an unreasonable valuation given the alternatives in bonds.

“The U.S. equity market has done quite well during the four years with Trump, despite increasing tension between the U.S. and China that has caused friction for U.S. companies around their global supply chains. Market participants are now used to Trump’s persona and the corporate sector has, in many ways, benefitted from Trump’s policies of lower taxes and less government oversight. Even the US-China relationship is to some extent predictable for companies and investors under a Trump administration.

“A Biden win, on the other hand, could become a headwind for equities as Biden has proposed to hike the statutory tax rate from 21% to 28% on corporate income and increase the Global Intangibles Low-Tax Income tax from 10.5% to 21%. In addition, Biden has proposed to hike the minimum corporate tax rate to 15% and add a social security payroll tax on high earners. Combined, it is estimated that these tax changes would create a 9% drag on S&P 500 earnings – and that is before second-order effects, including change in investor sentiment, potentially hit valuations. These would hit communication services, healthcare and information technology the hardest, as those companies have the lowest tax rates in general and are big users of intangible assets. The open question is whether Biden dares implement the tax changes during a weak economic backdrop.”

Commodities in a backdrop of a U.S. election and Covid

The combination of central banks actively supporting the return of inflation and the potential for the dollar to weaken further remains key to our general bullish outlook for commodities, especially those that historically have helped preserve wealth during times of raised uncertainty and inflation.

“The combination of Covid-related supply disruption, financial speculators looking for an inflation hedge and not least very strong demand from China driving down global stocks, have supported a strong year for industrial metals led by copper,” says Ole Hansen, Head of Commodity Strategy at Saxo Bank.

“Eventually, we see the steep uptrend in HG Copper from the April low being broken, leading to a period of consolidation which we believe may occur in Q4. On that basis, we see the short-term upside for copper as limited, with the potential driver for an extension being a renewed promise of infrastructure spending from the next U.S. president.

“Following a year where gold is up more than 20% and silver double that, it is a bold call to look for further gains. However, the powerful combination of rock bottom rates, rising demand for inflation hedges and the potential for a weaker dollar all point to further gains. Following a prolonged period of consolidation around and mostly above $1920/oz, we see gold eventually moving higher to finish the year at or near $2000/oz.

“The crude oil market is likely to remain stuck, with Brent crude spending most of the final quarter trading in the 40s before eventually moving higher into the 50s during the first half of 2021. On that basis, we raise our Q3 range by three dollars to a $38-$48 corridor. We remain cautious about crude oil’s short-term ability to rally much further, unless OPEC+ surprises the market by abandoning its planned 2 million barrels/day production increase set for January.”

USD bulls and bears may be in for a rough ride in Q4

The background going into Q4 looks challenging for any smooth continuation of the USD sell-off. U.S. political dysfunction and the risk of a contested election will have the market holding its breath. Post-election uncertainty, meanwhile, could drive a fresh spike in two-way volatility across markets and lead to many a false start for USD bull and bears, possibly into the New Year.

John Hardy, Head of FX Strategy, said: “The Fed and the U.S. Treasury’s twin howitzers of easing and enormous cash drops on the U.S. economy helped turn a spiking USD back lower. The USD sell-off began easing in late summer as the Fed stopped growing its balance sheet on a surprising strong growth rebound and the path to further fiscal stimulus was blocked. This theme is likely to persist for much of Q4. As Q4 rolls into view, the spectacle of the U.S. election dominates the horizon for traders across asset classes. The JPY might be a strong winner across the board in the worst-case scenarios for the U.S. election, and showed signs of coming to life after a long period of dormancy with the announcement of Shinzo Abe’s exit in September.

“A contested election is neither here nor there for the USD but gets more USD negative if the situation turns ugly and spills into 2021. And a narrow victory by either party without both houses of Congress is also USD negative as Congress won’t pass anything and the Fed will have to challenge the outer extreme of its mandate – and beyond – to support any recovery. Aside from the intense focus on the U.S. election and its implications for the U.S. dollar, the dominant issue hanging over everything is of course Covid-19. If vaccine candidates are not beginning to show promise at the end of 2020, we risk a deepening second dip in the global growth outlook. This will put an enormous dent in the reflationary narrative that purred to life in Q3, amid recovering commodity prices and support for commodity-linked currencies in EM and DM.

“The path to a traditional global reflation trade, driven by a weaker U.S. dollar and fresh credit cycle, will be frustrated as long as the virus continues to hold back the demand side of the economy and as long as fiscal authorities fail to force inflation high enough to outpace the real load of global debt.”

Getting Green Done

For the first time in the U.S. presidential election, climate change is emerging as a major theme. According to Professor Jon Krosnick, 25% of Americans will vote for a candidate based on their climate change agenda: a record high for the issue.

Christopher Dembik, Head of Macro Analysis for Saxo, said: “In mid-July, Joe Biden presented his ambitious climate plan worth about $2 trillion, or 2.5% of GDP, over four years.

“For the Democrats, the $2-trillion climate plan is both a way to address the impact of climate change on daily life and to create new jobs to offset losses from the pandemic. Its core goal is to reach carbon neutrality no later than 2050. The plan does not include a carbon tax at the federal level to contribute to reducing greenhouse gas emissions, but Biden does want to recommit to the 2015 Paris agreement, which aims to prevent the global temperature from rising more than 2°C above pre-industrial levels this century.

“This is the first time since 1972 that the Democrat electoral platform refers positively to nuclear energy as a way to be less dependent on fossil fuels. Going green with nuclear energy often raises public concerns about global safety and some question whether it is green enough to be part of a green new deal.

“Addressing climate change implies setting up the base of a green financial system that will be able to directly finance the Democrats’ ambitious green platform. Today, most ESG-related policies and regulations remain voluntary and are largely dependent on assets owners’ views on ESG investing. Under Biden, we see the emergence of new incentives to move towards stronger requirements, as is already the case in the EU.

“The Federal Reserve will have a very specific role to play in this new financial infrastructure and may integrate climate change across its mandates more explicitly – a process that has already started. It could take steps to favour green transition as part of its oversight of financial institutions, for instance via raising capital requirements for fossil energy project loans or lowering requirements for green ones.”

The Sovereign debt bubble poses threats amid U.S. election and rising inflation

As near-zero interest rates don’t give any protection against rising inflation, Saxo believes that sovereigns are the worst assets you can hold in your portfolio right now. Buying government bonds today means locking in such a low yield that, if inflation rises, the bond’s value will fall.

“Now more than ever, it is crucial to think about portfolio allocation and inflation hedges, to defend capital while we are witnessing a debasement of fiat currencies,” says Althea Spinozzi, Fixed Income Specialist at Saxo Bank.

“We believe that U.S. Treasuries today are the biggest mousetrap of all time. They do not provide any long-term upside, and the yield curve is doomed to steepen faster than expected due to inflation. Within the context of the U.S. election, however, there might be space for short-term trading opportunities. We anticipate a bull-flattener U.S. yield curve if Biden wins, and a bear-steepener if Trump wins. While the coronavirus pandemic has been beneficial to U.S. Treasuries and the Bund, the yields of riskier sovereigns jumped significantly. The most remarkable example is Italy, which at the moment is offering the lowest yield it has ever paid since joining the euro.

“If Trump wins, we favour financials, infrastructure, energy and domestic industrials and manufacturers. Junk bonds have a higher upside potential. However, even though we don’t mind lower-rated bonds, we still prefer mid-term maturities up to seven years to limit inflation headwinds.

“The market will perceive a Biden win as a credit negative. In this scenario, we prefer higher-quality bonds to take advantage of short-term volatility that will induce investors to fly to safety. We believe that the market has not priced a Biden win yet – this is why volatility will be high. Investors looking for longer-term investments should explore opportunities in the green bond space.

“There are also compelling opportunities both in the investment-grade space as well as the high-yield space within European corporate bonds. We find the lower investment-grade space and better-rated high-yield corporates to be the most interesting. A combination of central bank stimulus and economic recovery will favour bonds of those sectors that have been harshly hit by the pandemic.” In a complex fixed income market, cherry-picking and caution will reward investors. Although we see numerous challenges in the fixed income world, we believe that investors can still be successful in trading bonds.”

Bubble blowing not the answer

Saxo believes that a lack of courage to address structural inhibitors to diversified inclusive growth in the political sphere is leaving a legacy of worsening inequality and dividing American society. Time is ticking to fix capitalism before calls for socialist experiments grow louder thanks to shifting voting demographics.

Eleanor Creagh, Australian Market Strategist for Saxo, said: “Neither candidate has a vision that addresses rising inequality. Worse still, both the crisis itself and the policy response have supersized the problem. Not just via asset ownership, but via the pandemic’s uneven impact on certain sectors and industries: a dynamic coined the “K-shaped” recovery. Low-skill, low-wage workers who cannot work remotely face a depression-like environment. This is in stark contrast to the highflying technology sector, which has been accelerated by the pandemic.

“This broken economic model is depicted by fresh highs in stock markets out of touch with reality, contrasted with ‘Main Street’ where millions of Americans are still receiving unemployment benefits. With the second round of fiscal stimulus MIA, the ‘K-shaped’ recovery is in full swing – and set to worsen.

“The ‘have nots’ are now left behind by the political ideologies that historically would have supported their cause. This leaves vast swathes of the electorate feeling abandoned by both parties. In 2016, Trump used this opening to his advantage and adeptly spoke to those who had ‘lost their voice’, going after the middle of the country as an agent of disruption. With the economic playing field becoming more uneven, we cannot underestimate his capacity to do so once more.

“That is why this election cycle is perhaps more uncertain than ever. Human complexities, a lack of true leadership and deep-seated uncertainties held by individual agents about their role in the future of the economy will drive the popular vote. Notwithstanding the high probability of a contested result.”

Godzilla exits Japan = USD JPY 85-95, Tech Wars & Biden’s Asia Pivot

Japan’s one and only true modern-day Shogun in decades, Shinzo Abe, resigned in Q3 citing health. In addition to being Japan’s longest serving PM, Abe’s legacy will be centred around the orchestrated ‘Abenomics’ from late 2012.

“Firstly, despite what policymakers may say, with debt-to-GDP ratios of over 300% and the BoJ’s BS/GDP ratio of 120%, the bang for yen has expired way past its due date – especially considering Japan’s deflationary forces of a declining population and silver-haired demographics,” says Kay Van Petersen, Global Macro Strategist at Saxo Bank.

“Negative rates and YCC finally saw the yen cross the line. At 106, USD JPY today is around 15% below its all-time highs, but still some 35% up from the start of Abenomics. My view (in addition to be a mega-cyclical USD bear) is that for USD JPY, the highs are over and we are more likely to be below 100 (high 90s) than back above 110 before Q4.

“Could we see USDJPY in the 85 to 95 range by the end of 2021, as Abenomics unwinds? But the icing on the cake is that having short USD JPY exposure could potentially also be a great hedge if we run into market volatility linked to the US elections.

“Secondly, structurally speaking, Japan and the BoJ are at the endgame of what everyone else (including the Fed) is doing. The only difference is that the U.S. is four times the size of Japan, the Fed’s BS/GDP ratio is currently around 30% and the USD is a dominant global reserve currency. All this implies that we could be in for a greater than 150% run in the S&P and a much deeper depreciation in the USD, perhaps up to -30% from the 103 highs of the DXY over the next few years.”

Can we trust the 2020 US Election polls?

The election result in 2016 seemed to show a catastrophic error in the U.S. pre-election polls, triggering a great deal of forensic work on what went wrong. Investigations revealed that the national polls were actually quite accurate and correctly saw that Hillary Clinton would win the popular vote, with only a small deviation from the poll estimate. Specific state-level polls for Pennsylvania, Michigan and Wisconsin, however, were another matter. The polling averages for these three states showed Clinton with a solid lead. But they ended up going to Donald Trump by a razor-thin margin, making the difference in the election outcome.

Anders Nysteen, Quantitative Analyst at Saxo Bank, commented: “In nearly all U.S. presidential elections, the winner of the national popular vote also wins the Electoral College and thus the presidency. This also appeared to be the case in the days leading up to Election Day 2016, where forecasts gave Clinton around a 90% probability of winning the presidency, with a range of 71% to 99%.

“Polling organisations conduct surveys in different ways and through different media, and may thus be biased toward certain voter segments. They seem to be better prepared for the 2020 election, and are trying to learn from the pitfalls of their 2016 misses. Many of the errors above may be addressed by conducting thorough polling. One downside risk to this, however, is that it could result in polls which try to ‘overfit’ the 2016 scenario and may miss new developments specific to 2020. One new challenge is the Covid-19 pandemic, which may affect particular categories of voters more than others and may even lower overall turnout.

“So, when analyzing 2020 election polls, one should be aware of i) how the survey group was selected, ii) if the survey is asking for other parameters such as education and geography, and iii) if the polls also report the uncertainty in their predictions. This seems to be a minimum requirement for conducting a reliable 2020 election poll, and if these things are not specified, one should be extra careful about drawing important conclusions” concluded Anders Nysteen.