“Mind The Gap!” – The life and times of a man on the move Episode 50

Our fintech sector is far ahead of Apple and Facebook, Australian FX is totally safe regardless of the leverage and location restrictions, HSBC’s unwelcome lecturing vs its disruptive rivals clever approach, and mind your taxes!

In this weekly series, I look back on what stood out, what was bemusing, amusing and interesting during my weekly travels, interesting findings within the FX industry and interaction with an ever-shrinking big wide world. This is purely observational and for your enjoyment.

Monday: Big FinTechs, you can do it yourself!

From where I stood on the shores of the East Coast of the United Kingdom last week, a dialog with some of my longest standing colleagues who were en route by road to Harwich in order to go to Amsterdam for the Money 20/20 conference that took place that day were musing over the role of over reliance on what has become an internet dictatorship.

Following on from my rant, er, I mean opinion on Facebook’s deplorable attempt to launch its own unbacked and quite frankly unwelcome ‘currency’ into the hands of a general public which places too much trust on the social media giant which has delusions of grandeur as to its place in cyberspace and its role in being a pseudo-police force that is answerable to nobody and is able to spew its foul views onto its members and viewers, it appears that I am not alone in considering this move to be odious.

This subject reared its head once again during my casual dockside conversation at the Stena Line ferry port with people I have worked with for more than two decades as one of the key points to be discussed at the Money 20/20 conference on the other side of the water from Harwich was set to revolve around how FinTechs with substantial capital and a successful market share can partner with Apple and Facebook for digital services such as payments.

Desperation should never be part of any business plan, and my opinion on this is quite simple. Why would a new challenger bank with vast amounts of capital that have been hard-earned via its own genius seek dependence on a non-industry related counter-productive hater of the electronic financial services industry which banned all FX and CFD advertising in order to make way for its very questionable own digital currency?

Why trust a firm which chooses what it accepts for publication and what it doesn’t, is subject to no checks and balances, and downs a whole well organized, regulated fintech-based and central bank-backed industry’s potential client base so that it can offer a totally unreliable one of its own therefore putting its own members at risk by proxy?

Equal derision was apparent on the countenances of my earnest colleagues as was likely on mine, as to why fintech firms headed all the way to Holland, itself a massive epicenter of innovation and modernity, and then positioned themselves as attractive partners to ill-meaning dinosaurs such as Facebook, and looked to become possible takeover targets for firms such as Apple in their attempts to gain a slice of the trillion-dollar global payments market.

For those who have now been, seen and left, here is my two pennies worth for your $3 billion’s worth. Do it all yourselves!

FinTech shining lights such as OakNorth, a British digital bank that reached a $2.8 billion valuation earlier this year, is one example. It’s CEO, Rishi Khosla said at the conference that OakNorth is “in dialogue” with some tech companies over potential partnerships but wouldn’t specify which ones by name.

I hope these are new, modern tech companies that are able to help companies such as OakNorth and the plethora of other app based challenger banks and investing platforms that are now paving the way for the financial services sector of the future continue their quest in the right direction, that being safe, modern, fully integrated services that empower customers, and that firms this big and pioneering do not see themselves as so inferior to Facebook or Apple that they feel the need to rely on them for payment services.

A challenger bank with a $2.8 billion valuation is able to revolutionize the customer experience itself! The last thing it needs is Facebook’s anti-business approach hampering it.

We have seen this already in London as our sector begins to go the way of the modern, customer-focused app-based investing platform. Pipster is a prime example of this, its method being a modicum of empowerment for retail traders.

We, the electronic financial services sector, are the professionals who should be leading the way forward, and not curtailing the progress that is being made by relying on ne’erdowells like Mark Zuckerberg.

Tuesday: Deja-vu leverage restriction in Australia

Between my five annual trips to Australia, I think it is important to keep a close eye on pretty much every development that takes place there, from regulatory matters to technological and financial affairs, largely because Australia is one of the most respected and developed nations in the world for the retail FX and CFD business.

As a result, its importance on the map of the world for our industry is paramount and will always likely be.

Whilst calmness and shrewd acumen may well be two attributes that are notable in abundance within Australia’s retail FX sector, there has been a lot of discussion about the local regulatory authority’s attempts to follow Europe in its restrictive leverage, and to go one step beyond Europe in its attempt to curtail FX business to within its golden sand-covered shores.

I still maintain that ASIC’s draconian measure in forcing brokers to operate within national borders was a kneejerk reaction to lobbying from regulatory authorities in other regions, most of which are less advanced technologically and commercially, and certainly understand the internal structure of our industry a lot less comprehensively than ASIC does.

A look at ASIC’s highly sophisticated real-time surveillance system developed by First Derivatives over ten years ago when regulators in other regions were metaphorically still picking potatoes out of fields in terms of technological advancement, and then a listen to the incoherent ramblings of some of the heads of regulatory authorities that are responsible for the oversight of over 150 brokerages should be enough to discern which side of the equator regulatory knowledge of the retail sector is a abundant and which side it is lacking.

I have it on reasonable authority that ASIC is now looking to reopen its consideration of whether to restrict brokerages to Australian clients only, as this was a very sudden move that some lawyers and accountancy firms in Australia are under the impression was made with haste and is now under review to such an extent that it could be overturned.

This is especially an odd move given that most clients, whether corporate or individual, in the Asia Pacific region, Australia’s totally aligned trading partner business area, absolutely revere long-established, regulated Australian firms from the Tier 1 banks right the way to the retail FX firms, and so good is the partnership that brokers have built very solid and successful business on a carefully nurtured relationship, with absolutely no sign of detriment to either broker or customer.

Therefore, this measure perhaps came as a shock, but the potential leverage restriction that nobody really thought would take place should not be a surprise at all, and neither should it be anything to worry about.

Talking to a very good friend of mine on Tuesday about his tenure in the 1990s as a risk manager within Australia’s worldwide renowned derivatives business (Australia’s economy was pretty much founded on stock and commodities trading during the colonial mining period) it was clear that leverage has always been on the Australian government’s conservative agenda.

“In Australia, as I understand it, stock brokers used to offer margined trading in the form of stocks until CFD and FX margin brokers arrived in 2002” he said.

“Nowadays, there are margin lenders to stocks but at lower leverage, which usually means that for every $100 they can be lent $70” he continued.

“The thing to bear in mind here Andrew is that in the early 2000s, the business dried up for many margin stock brokers, because the CFD product was way superior and retail customers much preferred it. They still do” he said.

“This got me wondering about what the landscape was like in Britain before the advent of IG and CMC in the 1990s, or even in Europe, although I understand that Europeans were more to fixed income than equities” he mused.

“So maybe, and I am drawing a long bow here, with the new regulations to retail in Europe and abroad, it now opens up the stock brokers to offer similar products but in a more regulated and trusted environment, that is if stockbrokers are the same as they were in core business in the 1990s and 2000s because at least they can now compete in terms of product and leverage” he said.

I certainly agree that the CFD and FX OTC brokers absolutely disrupted the slow, latent and expensive exchange scene in Europe and Australia in the 1990s, which is why many of the exchange firms have been buying OTC derivatives companies.

Two years ago I met Stephane Boujnah, CEO of Euronext, Giorgio Modica, CFO of Euronext and and Lee Hodgkinson, Head of Markets and Global Sales and CEO of Euronext London, in which a series of questions and answers were posed live by senior industry executives across the world as Euronext bought Fastmatch, who told me that “FX is the absolute priority” however the firm has not become one of the major venues yet. That accolade goes to XTX Markets, which started off its entire business as a non-bank market maker, remains so today, and has more market share than the Tier 1 banks at the top level of FX dealing!

A close look at the mergers and acquisitions activity that has taken place among derivatives venues demonstrates two very important factors. The first is that the exchange venues, with their archaic modus operandi, and very expensive membership and clearing fees, are unable to maintain pace with technological advancement in terms of connectivity to live markets, platform responsiveness and ergonomics, and are way behind the prime of prime/prime brokerage price feed aggregation system used in OTC markets to bring efficient, live and real time trading environments to retail customers with far less latency than if a spot transaction was attempted via an exchange (the vast majority of exchange listed FX is futures – see Click 365, ICE, CME Group and Phillip Capital’s main volume generators in FX).

The second factor is that during the past two decades, the OTC sector has become so finely honed that it leads the way in terms of financial markets innovation, has garnered a longstanding and loyal retail customer base, often in domestic markets – most British CFD firms have 75% of their client bases within Britain – and the exchange sector is unable to gain its retail traders back via standard market competitive means.

The only methods that have been available to the giants of Chicago, Frankfurt and London in the exchange and equities sector has been through lobbying the regulators, and through aggressive mergers and acquisitions of FX specialists.

One of the first examples of this was CME Group which has been looking at a project whereby it comes up with a rolling spot contract which is a direct competitor to OTC derivatives firms.

Hotspot FX, one of the world’s most renowned OTC FX ECNs was bought by BATS Global Markets for $365 million in January 2015. It is also important to look at EUREX’s direction in which by September this year, the venue had extended its listed FX Futures and Options portfolio to include six new currency pairs while the overall minimum block trade sizes was reduced across all currency pairs to further improve hedging opportunities.

FinanceFeeds is also aware that this has been a focus for Deutsche Boerse for some time. Back in 2011, Deutsche Boerse took a minority stake in British FX technology solutions provider Digital Vega which was a technology vendor to buyside and sellside firms in the OTC derivatives sector.

At that time, the idea was to increase Deutsche Boerse’s positioning in the provision of pre-trade price transparency in the derivatives area for institutional investors and taking an initial footprint in the FX derivatives space. An investment agreement was signed last week, whereby Deutsche Börse will pay a US dollar amount in the single digit million range.

Deutsche Boerse bought 360T with the intention of moving the entire FX structure from an OTC bilateral system into an exchange clearing structure in my view. Another example of equity exchanges moving into FX was NASDAQ which wanted to launch NASDAQ FX but were unable to do so as they failed to understand the nuances of liquidty provision in an OTC trading environment vs the exchange traded products dynamics.

Where is all this now? Hundreds of millions of dollars in investment, and Hargreaves Lansdown, IG Group and CMC Markets still dominate the UK domestic market, and IG Group, Pepperstone, CMC Markets dominate Australia’s retail sector with INVAST Global dominating at prime of prime level.

This should pretty much be enough to answer any questions to the effect of whether the exchanges always feared the margin brokers and are unable due to legacy systems and legacy thought process to get the retail clients back without buying FX firms for a fortune.

An even keel remains in Antipodean OTC trading.

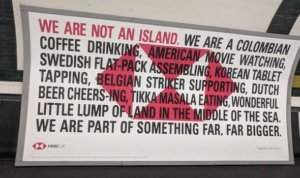

Wednesday: Now now, HSBC, practice what you preach….

There are times when I am very grateful that my car is compliant with London’s new Ultra Low Emission Zone regulations so that I can drive around the city listening to my choice of music via Spotify’ native app in the car’s audio system rather than be optically assaulted by some of the bovine excrement churned out by large companies advertising on the curved ceiling edges of the London Underground’s rolling stock.

As far as offline advertising is concerned, it is absolutely clear without even gaining access to statistics that the slots between the windows and the ceiling on London’s tubes are some of the world’s most prominent advertising space where a vast amount of material is memorized, and I have to say that in recent times, it’s the FX industry and the new app based challenger fintechs that are getting it right and coming up with some of the best, most witty, clever and original material.

Sadly, the Tier 1 banks are not anywhere near the level of our esteemed industry executives when it comes to making a clever point, largely because in the case of HSBC, an intrinsically British company which has its roots firmly planted in British colonialism in Hong Kong and mainland China, wit has passed their currently displayed diatribe by.

Rather than engage with its discerning customers, and let’s be fair, one of the reason that London Underground advertising is so effective is because literally millions of highly educated executives with massive business clout use the service every day, many of whom look up toward the adverts in order to partake in that very polite British pastime of not intimidating fellow commuters with eye contact. There is even a London Transport joke about that, which occasionally is stickered on the inside of carriages!

Nope, HSBC, instead of showcasing its brilliance, its latest tech and how it can compete with the Aritra Chakravartys of this world, himself a former senior HSBC FX executive who worked out that he could do a better job than his own employer despite its established status, and founded Dozens with massive support from recognized investors, HSBC decided to resort to politics.

HSBC’s anti-Brexit claptrap says nothing about the company other than it is an old colonial tweed jacket-wearing example of obsolescence, and one that does not stand by its own advice. HSBC will not be moving to Europe. It will be benefitting from the free WTO trade relationships between London, Hong Kong and Shanghai, its main three centers since its establishment.

It will not be moving clearing to Belgium, or Brazil, and it will not be making itself something far, far bigger, because it is already as big as it can possibly get and that relies on it operating from Canary Wharf, where all of the infrastructure, talent and hosting for the financial services business leads to and from.

One short sighted opinion from across the Channel is the supposition that the European Union’s hopes of bringing London’s financial markets sector to the mainland is as easy as taking business from London to Europe.

It is not that simple, as it would be impinged by approximately 8,000 miles of fiber optic cables which emerge from the seas around the UK at locations such as Crooklets Beach and Sennen Cove in Cornwall, and Highbridge in Somerset.

These cables carry data not only across the UK but to its continental neighbors, and whilst the European Central Bank is correct in suggesting that the majority of Europe’s critical infrastructure for trading FX, as well as shares and derivatives, is clustered in a 30-mile radius around the City of London, and that regardless of the UK’s future, some of the industry’s biggest data center operators, which host banks and high-frequency traders’ IT equipment, have announced capacity increases this year to cope with rising demand from investors in both Asia and the US, the real reason is not just infrastructural, it is really around why that level of infrastructure exists only in Britain and not elsewhere in Europe.

Britain’s interbank sector is responsible for 49% of all global FX order flow at Tier 1 level, and consists of British and international banks based in London, marking out London as a true free market, with no controls on which banks and non-bank entities (Thomson Reuters, Currenex, Hotspot all have centers in London) operate there, yet that is the de facto center for electronic trading and always will be.

For those who still have doubts, it may be worth asking Lord Myners how the proposed merger between London Stock Exchange and Deutsche Boerse worked out. Or you could ask me. I said from the beginning that it would never happen, and I was right.

Don’t lecture us, HSBC, sort out your own trade execution practices and be a leader in providing a global audience with what you actually are. A British, globally-orientated Tier 1 bank which is about to get into a global market once again, where it belongs.

Friday: WTH is WHT?

A brief note on some bureaucracy that is worth considering came to light on Friday, that being Europe’s new move toward the instigation of Withholding Tax on cross border commercial transactions.

This will not apply to traders, but it will apply to suppliers and customers of B2B services, for example a technology vendor looking to provide services to a broker which is based in a different country.

Poland has been the first European Union member state to put Withholding Tax (WHT) into force, however having spoken to a chartered accountant in London about this on Friday, all member states of the EU will follow suit.

Thus, for all firms wishing to keep this under control, you will need to obtain a “Certificate of Fiscal Residence” from the tax authorities in which your company’s main office and receiver/sender of remittances is registered.

Once that is obtained, it will need to be sent to all suppliers who operate in different countries to the company which is being supplied, in order that a 20% WHT is not applied to a supplier’s invoice meaning that the supplier would only receive 80% of the full invoice for services or goods, and even if the Certificate of Fiscal Residence is supplied at a later date, the 20% which would have been taken as WHT would not be reclaimable until the end of the next financial year.

My advice is to ask an accountant to act on your behalf, even though applying for a Certificate of Fiscal Residence is usually very easily completed via online methods because there are some bureaucratic anomalies that accountants are au fait with in terms of completing the form.

It is worth getting it in place now, because very soon all EU nations will be subject to it, as will Britain post Brexit. Hope this helps!

Wishing you all a great week ahead!