The Year-End FX Turn: To Everything There is a Season

By Paul Houston, Global Head of FX Products, CME Group

A time to every purpose: The year-end turn

The end of a calendar year typically sees an increase in U.S. dollar-based FX funding rates as cash is repatriated and applied to corporate and bank balance sheets. Further, the demand for U.S. dollars is often much higher due to non-U.S. borrowers satisfying dollar-denominated liabilities at year-end, creating strong forces which impact FX swap pricing. Therefore, it is said that FX swap activity, which crosses from one year to the next, incorporates “the turn” of the calendar year and reflects the seasonal dollar-demand phenomenon. Market participants, such as asset managers, who roll their OTC FX forward positions year-round are impacted during the year-end turn as they execute their normal roll activity. Some choose to roll earlier than usual and some get less choice in pricing as liquidity providers widen out or step back.

A time to build up: Data from CME Group markets on year-end funding

The data evidence is a bias to hold U.S. dollars over year-end, with funding pressure most pronounced approximately one week preceding year-end. The charts below present the interest rate differential as the excess USD rate over the opposing currency; a higher value shows higher U.S. dollar funding relative to the counter-currency. For example, using the January 2021 FX Link expiration, from December 1 to December 22, USD funding differentials increased by an average of 74 bps across the same G4 currency pairs of EUR, JPY, GBP, and CAD (ranging from 65 to 88 bps increase in differential). From the mid-December peak to the end of the first week of January, the funding differential dropped an average of -107 bps (ranging from -83 to -123 bps).

It is useful to contrast the year-end turn of 2020 and 2021. Financial conditions were relatively tighter during year-end 2020 as the world was still managing the effects of the COVID-19 pandemic; the Federal Reserve would maintain a target Federal Funds rate of 0 to 25 bps and purchase Treasury securities and agency MBS through mid-March 2022. As a result, the sharp increase in USD funding rates of year-end 2020 was not observed in year-end 2021, but the same seasonal pattern of falling USD funding rates through January was still observed. From the USD funding peak of December 15, 2021, through January 7, 2022, the implied rate differential fell by an average of -58 bps (ranging from -36 to -68 bps).

Given the material increase in inflation, both in and outside the U.S. (U.S. CPI reaching a year-on-year peak growth rate of 9% in June 2022), the Federal Reserve has responded forcefully. From the March 17 FOMC meeting where the Fed Funds upper bound was raised to 50 bps through the November 3 meeting where the upper bound was raised to 400 bps, the Fed Funds rate has gone up by an average 1.5 bps per day, including weekends[1]. Further, the size of the Federal Reserve’s balance sheet peaked on April 13 at $8.965T and has fallen by over $200 billion to below $8.7T[2]. This relative monetary tightness may create year-end funding strictures for non-U.S. participants.

The rate differential implied from FX swap pricing is distinct from the differential, which is observable from the zero-cross-currency basis pricing implied by CME SOFR and €STR futures[3]. Covered Interest Parity, Implied Forward FX Swaps, Cross Currency Basis, and CME €STR futures demonstrates how to use CME SOFR[HP1] and €STR futures to observe EUR/USD zero cross-currency-basis pricing and how highly liquid CME FX futures can be used to determine accurate forward FX pricing to transparently observe cross-currency basis prices.

A time you may embrace: Asset manager FX futures adoption and CME FX Link

Asset managers typically trade and roll their FX forward exposures against a panel of select bank liquidity providers. Given this, price discovery and access to liquidity comes from these relationships. As asset managers have sought to expand their ability to source liquidity, they have looked to FX futures. Asset managers are the largest customer category in CME FX futures: 42% of open interest in EUR futures, 39%, JPY futures, 35% of CAD futures, 28% of GBP futures[4]. Since the beginning of 2021, asset managers have added over 400,000 contracts, or $33 billion, in incremental open interest across the G4 currency pairs, growth of nearly 38% (both long and short)[5]. This asset manager adoption has led to record open interest and large open interest holders in CME FX futures in 2022, indicative of broad and increasing participation in CME Group’s liquid FX markets. Most participants roll their FX futures positions from one quarter to the next prior to each IMM-dated futures expiry. For G4 futures, up to 80% is rolled from one quarter to the next, on average[6]. This creates conditions for an active and robust order book for FX futures spreads where buyside natural interest, liquidity providers, and participants seeking liquidity for risk transfer come together.

In addition to FX futures calendar spreads, FX Link is a continuous FX spread traded on CME’s Globex central limit order book and is priced as the difference between a CME FX future and OTC FX spot. FX Link provides transparency through its firm and all-to-all model for eight currency pairs[7]. From FX Link pricing, one can observe real-time FX swap points based on the primary liquidity of CME FX futures[8]. Like FX futures, FX Link can be used as an alternative to expand liquidity choice.

Activity has grown substantially in 2022 to record levels as market participants embrace FX Link’s transparent pricing of FX swaps and the capital and balance sheet efficiencies afforded through clearing. Q3 average daily volume (ADV) of nearly 31,000 contracts / $2.8B was + 106% over Q3 2021. September ADV of over 46,000 contracts / $4.1B was +197% vs. September 2021.

For those with the ability to trade out U.S. dollars at year-end, FX Link provides a transparent, liquid way to manage year-end effects. This article demonstrates how FX Link can be used to enhance yield over observed interest rate differentials: Understand how the FX Swap Rate Monitor brings transparency to the FX swap market – CME Group.

FX swaps are the largest instrument in the FX market, comprising 51% of global FX turnover in April 2022, up from 49% in 2019. This growth is particularly notable as FX swap volume share increased in an overall increasing FX market. Total volume in OTC FX markets was $7.5 trillion per day in April 2022, up 14% from $6.6 trillion in 2019[9].

Bottom line:

- The seasonal effect to hold U.S. dollars over year-end is known as “the turn” and results in increased interest rate differentials between the U.S. dollar and other currencies. Participants who are not directly involved in the turn can be impacted as they roll their OTC FX forwards near year-end.

- Asset managers establish relationships with banks for OTC FX exposure; liquidity is a function of these relationships. Asset managers have materially increased their adoption of FX futures over time and are the largest customer category in CME FX futures, measured by open interest.

- FX Link provides transparent, anonymous, all-to-all pricing of FX swaps. The seasonal effect of increased U.S. dollar funding can be observed in FX Link pricing. FX Link can be used to manage year-end funding effects in forwards pricing in a way that separates credit from liquidity.

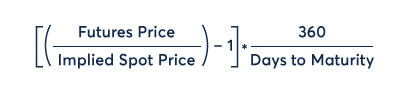

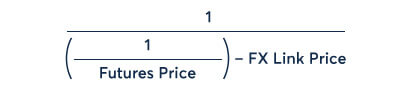

Appendix: Computing implied interest rate differentials from outright futures and FX Link prices

The implied interest rate differential is derived from the FX Link cash-futures basis spread and FX outright futures pricing as follows:

For futures contracts, which are quoted in line with OTC convention (EUR, GBP, AUD, and NZD), the implied spot price is simply the difference between the futures price and the FX Link price. For futures contracts that are quoted inversely to OTC convention, the implied spot price is derived from the inverted futures price, and inverted to align with the futures price convention to express the rate differentials as the excess USD rate over the non-USD rate:

The subject matter and the content of this article are solely the views of the author. FinanceFeeds does not bear any legal responsibility for the content of this article and they do not reflect the viewpoint of FinanceFeeds or its editorial staff.