RHT Compliance Solutions in Singapore provides Compliance and Risk Advisory to Financial Institutions and Capital Market Intermediaries in Singapore and the region. They will offer Muinmos’ proprietary Regulatory Onboarding Engine to their rapidly growing client base which includes banks, investment banks, brokers and fund managers.

Muinmos’ innovative technology uses AI and machine learning to simplify onboarding and enhance the compliance process across multiple jurisdictions. Its Regulatory Onboarding Engine comprises three distinct and secure modules, mPASS™, mCHECK™ and mRX™, to provide flexibility to Financial Institutions. When combined, these modules provide a complete one-stop-shop regulatory compliance onboarding solution.

mPASS™, specially developed for automated categorisation, suitability and appropriateness checks, provides instant clearances on whether Financial Institutions can onboard or keep a client in any country / for any financial service and financial instrument. Clients can be fully cleared and ready to be onboarded in under three minutes.

mCHECK™ covers all relevant AML/KYC requirements, and mRX™ is a risk management tool enabling Financial Institutions to risk profile their clients based on their pre-configured risk parameters.

As regulatory parameters change, Financial Institutions are instantly alerted of any regulatory change or even potential new sales opportunities. This ensures ongoing 24×7 compliance across the globe whilst mitigating the risk of fines and mis-selling.

Jayaprakash Jagateesan, CEO, RHT Compliance Solutions comments, “The timing of this partnership is ideal. The Government in Singapore is encouraging firms to embrace technology and go digital. Financial Institutions are looking to automate processes wherever possible and Muinmos’ RegTech products are ideally placed to help the compliance function to become more streamlined and efficient. We are excited to bring this technology to our clients.”

“Muinmos’ products complement our existing services. We are certain, for example, that the regulators will be impressed by our clients who are applying for licences if they can see that these firms will be using such a powerful onboarding tool to enable them to meet their regulatory requirements. Through our partnership with Muinmos, RHT can offer a one-stop-shop for regulatory compliance including advisory services, customised training, preparation for regulatory inspections and advanced technology solutions.”

Remonda Kirketerp-Moller, Founder and CEO, Muinmos adds, “We are delighted to be working with RHT Compliance Solutions. With our regulatory onboarding product and RHT’s deep local expertise and network, I believe we have a powerful combination and the ability to put RegTech firmly on the map in Singapore. Together, we can help Financial Institutions in Singapore and beyond to digitise their compliance processes and be safe in the knowledge that they are adhering to regulatory requirements throughout the lifecycle of their clients.”

Muinmos’ proprietary Regulatory Onboarding Engine maps thousands of regulatory parameters, legislation, permissions, rules and guidelines from around the world and delivers instant compliance results globally. For further information, visit www.muinmos.com

RHT Compliance Solutions is the first and only integrated organisation providing Compliance and Risk Advisory to Financial Institutions and Capital Market Intermediaries in Singapore and the region. RHT Compliance Solutions is a subsidiary of RHT Fintech Holdings, a leading Professional Services Group in Asia. For further information, please visit, www.rhtgoc.com

During the year the organization achieved several records in its operations metrics including the number of filed complaints (1340 complaints – 32% increase YoY), amount of compensations souпре by traders ($10.9M sought by all traders – 48% increase YoY), and awards to traders ($1,495,474 awarded to traders – 148% increase YoY) while keeping one of the fastest dispute resolution timeframes in 6.97 days per dispute

Other key metrics & accomplishments in 2020

$8,812 average complaints value – 20% growth YoY

$8.1M sought from member brokers – 248% growth YoY

31% YoY increase in complaints ruled in favor of traders

6.97 days average dispute resolution time – 3% increase from 2019

Key Takeaways

The Financial Commission keeps expanding its international presence with the addition of 12 new approved broker members to its membership ranks and certification of a new education provider, while also adding a new member to its Blockchain Association. In 2020 the organization also set several strategic partnerships with The Industry Spread media portal and one of the biggest liquidity providers – Advanced Markets. The Commission’s Dispute Resolution Committee was also strengthened by two new experts from Europe and Turkey

Regional Presence

The organization further expanded in the Middle East, with several new Turkish broker members, as well as the addition of a Turkish expert on the Dispute Resolution Committee. The organization’s free dispute resolution service to traders gained popularity in Asia, the Middle East, and Africa with new complaints from these regions growing 202%, 15%, and 14% respectively in 2020. The Financial Commission also saw a 17% decrease in complaints from Russia and former Soviet republics, as local market restrictions impeded the normal online trading operations FX and CFD traders have come to expect.

Complaints Highlights

The majority of complaints received by the FinaCom in 2020 were related to financial issues with 55% of the total, while trading related disputes accounted for 25%. The most popular topics for complaints dealt with funds withdrawal (31%), agreement breach (17%), price check (14%), and account blocking (6%). Of all resolved complaints, 52% were resolved “in favor of the broker” and 18% resolved “in favor of the client”, while 30% were found to be outside the organization’s jurisdiction.

About Financial Commission

Founded in 2013, the Financial Commission is a leading independent member-driven external dispute resolution (EDR) organization for international online brokerages, exchanges, and Blockchain firms that participate in global foreign exchange (forex), derivatives, CFD, and digital asset markets.

The Financial Commission provides efficient compliance solutions to its members, alongside its External Dispute Resolution (EDR) mechanism that serves as an effective channel for processing complaints from clients of member firms.

Below is AxiCorp’s statement regarding today’s announcement by ASIC regarding their AFS license:

“AxiCorp Financial Services Pty Ltd can confirm that on 2 January 2020 the Australian Securities and Investments Commission (ASIC) made a decision to suspend our Australian Financial Services Licence (AFSL). While we respect ASIC’s view, we have appealed the decision to the Administrative Appeals Tribunal (AAT) and will be contending that a suspension was not the correct decision.

The AAT has “stayed” the operation of ASIC’s decision. This means that the suspension of our AFSL will not have any effect until the AAT has reviewed and finally determined the matter.

Until the process has concluded, our Australian clients are still able to trade as normal and we are still able to service new clients. Clients trading through other AxiCorp entities are unaffected by this decision and can also continue to trade as normal.

We strongly believe that the issues raised by ASIC are generally historical, in many cases self-reported and do not deserve a suspension, which is why we’ve appealed the decision.

AxiCorp has made significant investment in its Australian compliance function and practices to ensure it is appropriate to meet our obligations with reference to the size and complexity of the business.

In fact, we’ve recently commissioned an independent review by a highly experienced and qualified risk management and regulatory compliance expert in relation to ASIC’s concerns. The report (shared with ASIC) made a number of positive observations about AxiCorp’s compliance operations, highlighted some areas that required further work. AxiCorp has completed all of the work required and has taken steps to address the opportunities for further improvement identified by the expert.

AxiCorp entities also remain licenced by top tier regulators, including the UK Financial Conduct Authority (FCA) and the Dubai Financial Services Authority (DFSA), and we take our regulatory obligations in all countries extremely seriously.

We are a well-capitalised company and our clients are consistently the most satisfied with our overall service, including trade execution, compared to our major AFSL entity competitors.

Globally we continue to strong growth in active clients, trading volume and revenue, and are firmly established as a top 10 retail Global FX/CFD Broker – a reflection of the quality and transparency of the award-winning service we provide to our valued clients”.

Cappitech, a leading provider of regulatory reporting and intelligence technology for the financial services industry, today announced the results of a survey of over 100 European buy- and sell-side compliance decision-makers. The survey examined how MiFID II regulation has affected financial services organisations and how these plan to tackle new regulations such as Best Execution and RTS27/28 in order to improve their business processes.

The Cappitech survey found that, despite a legal obligation to comply with Best Execution under MiFID II, 65% of respondents do not monitor trades systematically according to best execution criteria. Furthermore, almost 60% of respondents have no plans to use their Best Execution reports internally, even though the data would improve their execution quality, client offering and ability to make better informed business decisions.

“Many firms still don’t define their best execution policies properly, and many of those that do so don’t have a system to monitor their policies in a systematic fashion,” said Ronen Kertis, CEO and Founder of Cappitech. “Furthermore, the operational processes in many cases continue to be unnecessarily laborious and complex. Industry participants need a single point for all compliance needs across reporting, execution quality analysis, service, ARM and Trade Repository integration and reconciliation.”

Additional Survey Findings

More than half of the respondents were not fully compliant with MiFID II’s reporting mandates on January 3rd this year, confirming industry-wide suspicions that large numbers of market participants were struggling in the run-up to the implementation date.

Firms are still unclear about which financial instruments fall under MiFID II’s purview from a transaction reporting perspective. ESMA’s Financial Instrument Reference Database (FIRD), conceived to help firms understand their reporting obligations, is complex and confusing.

Firms that rolled-out new technology prior to the MiFID II deadline might be paying too much for TCA solutions, which in many cases feature unnecessarily broad functionality, designed expressly for bulge-bracket firms.

To see the full survey results, download the report or view the summary infographic.

Moscow Exchange (MOEX:MOEX) announces it has signed a statement of commitment to the FX Global Code, pledging to support robust, fair, liquid, open and transparent foreign exchange markets.

The FX Global Code (Global Code) is a set of global principles of good practice in the foreign exchange market, developed to provide a common set of guidelines to promote the integrity and effective functioning of the wholesale foreign exchange market. It was developed by a partnership between central banks and market participants from 16 jurisdictions around the globe.

“We endorse the FX Global Code and are committed to the highest levels of fairness and transparency,” said Igor Marich, a member of MOEX’s Executive Board and Head of the Money and Derivatives Markets.

“As the world’s largest liquidity center for the ruble, Moscow Exchange has a special responsibility to operate an open, resilient and trustworthy FX trading platform. By committing to the Global Code, we are ensuring our practices are aligned with leading international standards and our infrastructure will remain robust and reliable.”

Moscow Exchange joins more than 100 other market participants in confirming its commitment to the Global Code, including central banks, banks including Barclays, Citi, Deutsche Bank and JPMorgan Chase & Co and electronic trading platforms such as Bloomberg and Thomson Reuters. Moscow Exchange is the first Russian financial institution to commit to the Code.

Moscow Exchange is the global center of liquidity for the ruble and hosts trading in 10 currency pairs including its most traded Russian Ruble/US Dollar pair. In the first half of 2018 the average daily trading volume (ADTV) on Moscow Exchange’s FX Market across all currency pairs was equivalent to USD 23.6 billion. Though today the most diversified exchange globally – offering trading in stocks, bonds, futures & options, FX, money market products and commodities as well as clearing and depositary services – Moscow Exchange was founded in 1992 as the Moscow Interbank Currency Exchange (MICEX) and in its early years was exclusively a currency trading venue.

Moscow Exchange first announced its intention to join the Global Code in January 2018.

ASIC has accepted a court enforceable undertaking from Goldman Sachs Australia Pty Ltd (GS Australia) to improve controls relating to bookbuild messaging in certain equity capital market transactions lead managed by GS Australia. A bookbuild is the process of generating, recording and capturing demand from potential investors for a capital raising transaction.

Following an investigation into a block trade transaction undertaken by GS Australia in relation to shares in Healthscope Limited on 23 November 2015, ASIC had concerns about certain representations made by GS Australia to potential investors about the minimum fixed demand.

GS Australia has implemented changes to its controls and processes including to require:

legal or compliance approval of all bookbuild messages to be provided to potential investors in certain equity capital market transactions; and

compliance attendance at any sales calls at the launch of certain equity capital market transactions to provide oversight of messaging to potential investors.

Under the enforceable undertaking, GS Australia will conduct an internal review of policies, procedures, systems, controls, training, guidance and the monitoring and supervision of employees engaged in equity capital market transactions lead managed by GS Australia and which involve a bookbuild or underwriting process, and implement changes to address any deficiencies identified.

Following those changes, GS Australia will provide an attestation from a senior executive to ASIC that the controls are adequate and appropriate to address ASICs concerns.

GS Australia will also make a community benefit payment of $500,000.

ASIC Commissioner Cathie Armour said “This court enforceable undertaking reinforces our focus on intermediary conduct and standards in capital raising transactions. Investors need to have confidence that they are being provided with accurate information in the course of a bookbuild or underwriting process.”

GAIN Capital Holdings, Inc. (NYSE:GCAP) notes that the European Securities and Markets Authority (ESMA) and the Financial Conduct Authority (FCA) have issued statements announcing regulatory changes in the provision of contracts for difference (CFDs) to retail clients.

The measures on CFDs are being introduced as a temporary intervention on a three-month basis, during which ESMA and FCA will reflect on whether it is necessary extend the intervention measures for a further three months or on a permanent basis, respectively.

While GAIN does not agree with every aspect of ESMA’s new rules, the Company is strongly supportive of measures that enhance consumer protection in the FX/CFD market and elevate standards across the sector, including curbing aggressive marketing to inexperienced investors and mandating disclosure requirements that ensure all clients fully understand the risks of FX/CFD trading.

GAIN operates a diversified business, which includes a retail FX/CFD business spanning eight regulatory jurisdictions, a U.S.-based retail futures business and an institutional trading business. As a result of this diversification, as well as due to actions being taken by the business to mitigate the impact of ESMA’s proposed regulations, the Company believes that ESMA’s new regulations place less than 5% of full year 2018 total revenue at risk, based on an anticipated implementation date of the end of the second quarter of 2018.

The Cyprus Securities and Exchange Commission (“CySEC”) has today imposed a financial penalty on ICFD Ltd (the “Company”), an investment firm that provides online retail trading products in forex. A fine of €138,000 has been imposed on the Company for multiple compliance failings.

These failings that occurred in 2016 breached the policies and procedures CySEC enforces on Cyprus Investment Firms (“CIFs”) in order to guarantee full investor protection.

The identified failings included a non-compliance with:

Section 6(8) of the Investment Services and Activities and Regulated Markets Law of 2007, as amended (‘the Law’),

Section 28(1) of the Law, as it failed to comply, at all times, with the authorization and operating conditions laid down in sections 18(2)(a) and 18(2)(d) of the Law, as specified in paragraphs 14 and 16 of Directive DI 144-2007-01 of 2012 of the Securities and Exchange Commission for the Authorisation and Operating Conditions of CIFs (“Directive 1”),

Sections 36(1), 36(1)(a), 36(1)(b) and 36(1)(d) of the Law and paragraphs 4, 6, and 16 of Directive DI 144-2007-02 of 2012 of the Securities and Exchange Commission for the Professional Competence of Investment Firms and the Natural Persons Employed by them (“Directive 2”).

In non-compliance with these regulatory obligations, the Company’s specific failings concerned:

The Company provided investment services it was not licensed to offer by CySEC, including the investment advice itself;

The Company did not take reasonable steps to avoid operational risk deteriorating when running its business and/or when outsourcing activities to third party service providers;

The Company did not act fairly, honestly and professionally to serve the best interests of its clients at all times;

In providing information addressed to clients and potential clients from employees of its call centres, the disclosure on the Company’s website, and the contents of the Company’s advertising was not clear, accurate and not misleading. These materials consistently failed to alert clients and potential clients to the risks of and warnings in investing;

In providing information addressed to clients and potential clients, the Company failed to ensure it sufficiently communicated the nature and risks of the investment service(s) offered;

The Company was therefore unable to assess whether the proposed investment service or financial instrument provided to them by the Company was suitable for these clients;

The Company did not source or collect the necessary information from its clients and potential clients regarding their relevant knowledge and experience to trade in the particular financial products it was offering;

Further, the Company encouraged clients and potential clients to not provide the information required for the purposes of Article 36(1)(d) of the Law, in demonstrable violation of the explicit legislation.

In addition to the financial sanctions imposed on the Company, CySEC has also enforced a number of corrective actions, in respect to the above deficiencies, to ensure full compliance with the Investment Services and Activities and Regulated Markets Act of 2017 (Law 87(I)/2017), which entered into force on 3 January 2018 and harmonises the Cyprus legal framework with Directive 2014/65/EU on Markets in Financial Instruments (MiFID II).

Demetra Kalogerou, Chair of CySEC, said:

“Following CySEC’s investigation, the Company was found to be in violation of the laws we have in place and enforce to protect retail investors trading in speculative financial products, such as forex. The Company in question showed, among others, deficiencies in properly disclosing the risks to existing and prospective investors, and in some cases, even served to promote and actively market certain products at the expense of providing clear and non-misleading information. Having enforced a number of corrective measures in addition to those financial penalties imposed on the Company, CySEC will continue to keep the Company under close supervision and it will remain subject to follow-up inspections.”

The Cyprus Securities and Exchange Commission (CySEC) today announces that it has imposed a financial penalty on Spot Capital Markets Ltd. (the “Company”), an investment firm that provides online retail trading products in forex.

A fine of €50,000 has been imposed on the Company for multiple compliance failings that occurred in the period between 1 January 2016 and 30 June 2016 that breached the policies and procedures CySEC enforces for investment funds and their third party service providers in order to guarantee full investor protection, including:

€30,000 for non-compliance with Article 36 (1) (a) of the Law and paragraph 6 (2) of Directive 2, for failing to communicate with customers and potential customers in an accurate, clear and non-misleading manner as required under the law. The Company failed to ensure that its third party service providers entrusted with the promotion of the Company’s services met the required standards as set out in Article 36 (1) (a) of the Law;

€20,000 for non-compliance with Article 36 (1) (a) regarding the Company’s offering of financial advice, which was found by the Internal Auditor to be against customers’ best interests.

The Company, its account managers and third party telephone service operators were found to not be acting fairly, honestly and professionally to best serve the Company’s customers’ interests. CySEC treats the propagation of inappropriate and misleading financial advice very seriously. Investment advice offered by unauthorized individuals, or misleading investment advice that is not given with the customers’ best interests as principal is treated as a most severe breach of the rigorous laws enforced by CySEC concerning customer protection. With regards to Spot Capital Markets, this included giving false reassurances of promised or guaranteed profits, and inciting customers to deposit more money within the Company in order to cover potential losses. Finally, the Company and the service providers it contacts – and is responsible for – offered false guarantees of the safety of customers’ money.

When deciding the amount of administrative sanctions levied on the Company, CySEC took into account the seriousness of the CIF’s obligation to act fairly, honestly and professionally to best serve the interests of their clients. In mitigating the financial penalty imposed, CySEC accounted for the Company’s corrective actions implemented under CySEC’s jurisdiction. This included measures taken by the Company to change the information sent to customers, and significantly improving compliance regarding interactions with customers by providing training to staff of both the Company and of third party service providers.

CySEC also took into account that this failing was the Company’s first breach of the law, and that the Company has made changes in the composition of its Board of Directors.

Demetra Kalogerou, Chair of the CySEC, said:

“The Company and its third party service providers did not meet the rigorous standards prescribed by the laws we have in place to protect investors. Investment advice and information provided by CIFs allows customers to make informed decisions. CySEC legislation is clear that this advice and information, as provided by CIFs or third party service providers under the authority of CIFs, must be in customers’ best interest. Since CySEC’s investigation into the suspected failings of the Company, and subsequent administrative fine, Spot Capital FX has taken substantive measures to rectify the language of their financial advice, improving their overall compliance.”

SafeCharge (AIM:SCH), payment technologies provider, today announces that its wholly owned UK subsidiary, SafeCharge Financial Services Limited, has been authorised by the Financial Conduct Authority (the “FCA”) as a Payment Institution. This in in addition to SafeCharge Limited’s existing authorisation as a European Electronic Money Institution.

The authorisation will allow SafeCharge Financial Services Limited to provide payments services in the UK in accordance with the Payment Services Regulations. It will enable SafeCharge to continue expanding its services portfolio to its existing client base and to new clients, as well as future proofing the business post Brexit and potential changes to the passporting rules.

David Avgi, CEO of SafeCharge, commented:

“Obtaining the Payment Institution license from the FCA fulfils one of our central objectives, as outlined in our strategy. It is also an independent endorsement of our best practices in Risk management, KYC, AML and Compliance and is testament to our high operational standards. Our merchants now have the additional validation and confidence provided by the FCA authorisation.

This license places SafeCharge in a key position to capitalise on the expansion of its business and services in the UK market and other EEA members.”

CMC Markets Plc (“CMC” or “the Group”) notes that the Financial Conduct Authority (“FCA”) has today issued a letter to providers and distributors of contracts for difference (“CFD”).

Positive steps have already been taken by the Group to address the points raised in an individual letter received from the FCA in September 2017 and in conjunction with CMC’s MiFID II preparedness. CMC continues to focus on its target market and works closely with its small number of distributors to enhance regulatory compliance.

The Group welcomes the application of strong and consistent regulation across the industry, to achieve fair client outcomes and does not believe that these findings will have any additional financial impact on the Group.

Following today’s letter by the UK Financial Conduct Authority (FCA) to providers and distributors of contracts for difference (CFD) products, online trading major IG Group Holdings plc has filed its response to the document.

IG welcomes the FCA’s review on the provision and distribution of CFD products to clients on an advisory or discretionary basis. IG does not offer advisory or discretionary services for CFD products and has terminated its very small number of relationships with distributors who offer our CFD product on a discretionary or advisory basis to retail clients within the UK and EU. IG believes that it complies with the applicable rules and FCA guidance and that this review has no new financial implications for IG’s business.

“The Company is always seeking to improve and we have taken steps to address the observations made by the FCA in their individual letter to IG on this aspect of the industry in October 2017. We believe that stricter supervision of those firms who do not comply will lead to improved client outcomes in the industry”, IG said in its response.

In line with RPPD and MiFID II product governance obligations, IG has carefully defined its target market. This is shared with the few partners with whom IG works, and who distribute its products in accordance with IG’s own high standards.

The Company has delivered a sustainable business by placing good client outcomes at the heart of everything it does. Good conduct, from the way products are designed, to how they are marketed, to whom firms allow to use them, is essential in protecting clients.

The Company’s long held view is that robust supervision around who the product is marketed to, and which applicants are accepted as clients, remains the most significant measure to drive improved client outcomes.

HM Treasury has today announced the appointment of Charles Randell CBE as the new Chair of the Financial Conduct Authority (FCA).

Mr Randell is currently an external member of the Prudential Regulation Committee of the Bank of England and a non-executive board member of the Department for Business, Energy and Industrial Strategy. He will take up the role on 1 April 2018. The appointment is for a five year term.

John Griffith-Jones, Chair of the FCA commented:

“I am delighted that Charles Randell has been appointed as my successor and I wish him every success in the role.”

Andrew Bailey, FCA Chief Executive commented:

“I am very pleased to welcome Charles to the FCA. His experience of regulation, both during the financial crisis and more recently as a member of the Prudential Regulation Committee, mean that he has a strong understanding of the challenges that the FCA faces and I look forward to tackling these with him in his new role.”

Charles Randell worked at Slaughter and May from 1980 to 2013, becoming a partner in 1989. He specialised in corporate finance law, and worked on financial stability and bank restructuring assignments.

He advised HM Treasury on the resolutions of Northern Rock, Bradford & Bingley and the Icelandic banks; the Government’s investments into RBS and the merged Lloyds/HBOS; and the Asset Protection Scheme. Mr Randell also advised the Portuguese Ministry of Finance on the recapitalisation of the Portuguese banking sector.

Mr Randell is a member of the Prudential Regulation Committee of the Bank of England; a Non-Executive Director and Chair of Audit and Risk Assurance Committee, Department for Business, Energy and Industrial Strategy; and a Visiting Fellow in financial services regulation at Queen Mary University of London.

Financial Commission, an External Dispute Resolution (EDR) organization, operated by FinaCom PLC, servicing online Forex and CFD brokerages and technology providers within the financial services industry, today announces the appointment of Alexey Sidorov to its Dispute Resolution Committee (DRC).

Alexey Sidorov is the latest industry expert to join the Financial Commission’s DRC – which consists of a diverse panel of industry professionals, who follow a non-bias protocol to process and resolve complaints from the Financial Commission members’ clients.

Alexey Sidorov – Chairman of the Financial Market Development Association of Belarus (ARFIN) is a prominent financial markets economist with senior-level executive experience which includes serving for private companies and governmental financial institutions over a career spanning over 17 years.

Mr Sidorov was Deputy Head of the Department for Foreign Economic Activities Monitoring at National Bank which drafted legal regulatory acts under the main directorate for currency regulation and currency control. He held this role from 2013 through June 2016, and his work involved monitoring foreign trade activities and drafting appropriate regulations to meet policy needs as Deputy Head of the department.

Before his promotion to the role of Deputy Head, Mr Sidorov was Chief Economist at National Bank, for eight years from 2005 through 2013, and during that time was an adviser for the currency regulation department within the main administration of currency regulation and currency control. This department drafted legal acts and maintained existing rules for currency regulations and under his guidance.

Prior to joining National Bank, Mr Sidorov was senior economist at Infobank (JSCB) at the active operations department which managed the bank’s loan portfolio and sale of banking products.

He studied at the Belarusian State Economic University in the Faculty of Banking with a specialization in finance and credit, from 1997 to 2002, before embarking on his career in finance.

Peter Tatarnikov, Financial Commission Chairman, said “We are extremely pleased to welcome Alexey Sidorov to the Financial Commission’s Dispute Resolution Committee. Alexey is a proven leader who has held several top level positions for governmental regulatory institutions in key roles relevant to Forex regulations, and also brings valuable experience from in the banking sector as an economist.”

Image: Financial Commission Chairman, Peter Tatarnikov, and ARFIN Chairman, Alexey Sidorov

FinaCom PLC, operator of the Financial Commission (FinancialCommission.org) – an independent self-regulatory organization and external dispute resolution (EDR) body for the online trading industry including FX and CFD market participants, retail financial consumers, brokerages, and technology providers, today announces the results of its 2016 Annual Report.

2016 Membership Growth, New Appointments, Key Events and Industry Observations

Financial Commission’s 2016 annual report recaps another year of continued growth. As the number of approved membership applications increased during the year, so did the number of complaints that were filed with Financial Commission during 2016.

There was further expansion from new appointments to the Dispute Resolution Committee (DRC) and significant cross-border synergies with other regulatory and non-governmental organization (NGOs), as well as meetings with foreign regulators and industry event participation in Europe and Asia where key Industry themes were observed and collected from market participants’ feedback.

Key Industry Themes During 2016

Several key industry trends persisted during 2016 such as the importance of self-regulatory efforts in the field of best-execution practices as the FX Global Code initiative was underway and brought the subject of fair dealing practices further under the spotlight, and as a voluntary code of conduct was rolled-out for interbank dealers.

A global derivatives survey by IOSCO in 2016 coincided with a growing wave of reforms against binary options providers and helped to set in motion efforts to seek a clear framework for how margin FX and CFDs are offered across various jurisdictions. These efforts paralleled a reduction in leverage implemented by several regulators following the aftermath of major events including the UK’s Brexit that caused unprecedented volatility in the GBP/USD currency pair in 2016.

Despite the shockwave from these 2016 events including Brexit and major geopolitical shifts from Trump’s victory in the US election, global markets including foreign exchange functioned efficiently with many brokers taking prudent measures to prevent against market gaps by voluntary reducing leverage and limiting trading on a number of occasions, reflecting self-regulation at its finest.

Financial Commission 2016 in Review

On the backdrop of challenging market conditions, Financial Commission was well positioned to handle a significant increase in the number of complaints together with the addition of new members, as factors such as trading volumes and volatility ranged from low to high surrounding major events throughout 2016 and which led to considerable changes in asset values for active and passive market participants.

Whether due to volatile market conditions or from the normal course of day-to-day operations, disputes may arise between customers and their broker from time-to-time. When such grievances cannot be amicably resolved, a formal complaint is filed with Financial Commission – where it is then examined using a systematic approach and is fully investigated before being reviewed by the DRC to render a non-bias decision. Using a proven dispute resolution process, Financial Commission achieved another record year across the board during 2016 including the following key highlights:

2016 Highlights

There were 165 complaints filed with Financial Commission, a nearly 80% increase compared to 93 complaints filed in 2015.

There were 4 new appointments made to bolster the Dispute Resolution Committee.

A total of eighteen new members were approved by Financial Commission which brought the total number of members to thirty-three, including certified technology providers.

Financial Commission participated in key industry events across the globe, meeting with clients and members at important industry conferences in Hong Kong and Cyprus, and held important meetings with industry regulatory bodies in Eastern Europe.

About Financial Commission

Financial Commission operates as an independent EDR using a membership-based structure and is not a governmental organization or sanctioned by any jurisdiction, and is domiciled in Hong Kong under FinaCom PLC. The ethos of our mission statement is transparency, swiftness, and education, which are the paramount drivers that uphold our operations.

Supporting self-regulatory efforts is just one of the benefits provided by the Financial Commission to its members who join voluntarily – yet must adhere to strict guidelines in order to maintain membership and demonstrate transparency, compliance, and integrity to their customers.

The Financial Commission helps intermediate fair dealings by providing an unparalleled dispute resolution process between online brokerages and their end-customers, in the rare but inevitable cases of trade disputes that cannot be resolved.

The subject of each complaint can be as diverse as the underlying broker, product, or customer, yet all disputes share one thing in common which is to seek fair dealings regardless of the financial services products, providers, trading technologies, or pricing issues related to market participants’ transactions, from the complaints that are filed.

Financial Commission guarantees protection of the interests of both brokers and traders, thus is providing a fair and neutral platform to effectively resolve complaints. Financial Commission ensures that traders and brokers are getting their disputes resolved in an efficient, unbiased, authentic, and a quick manner and walk away with a well-founded answer.

Details of 2016 Results

Below the Commission presents further details of its Annual Report for 2016, which also provides statistics on the number of complaints handled and key metrics regarding processing and mediation results. The statistics information is insightful to our Members and their clients, the public, and for brokerages that are considering the benefits of obtaining membership with the Financial Commission and/or are interested in learning about the organization’s structure.

2016 Complaint Statistics in Review

The need for transparency continues to grow. Building trust is crucial and using fair and neutral 3rd party dispute resolution – that Financial Commission provides – is an effective solution in cases where clients or brokers cannot resolve matters together and seek an independent channel and wish to avoid often complex legal or costly arbitration alternatives. The Financial Commission continues to achieve this objective by providing brokerages and technology firms with the benefits that accompany membership status, as seen in the statistics results for 2016.

A significant increase of 77% was achieved in the total number of complaints received in 2016 (165 complaints filed), compared Year-over-Year from 2015 (93 complaints filed). This nearly 80% increase was driven from the addition of new members reflecting the increasing credibility and positive reputation Financial Commission has been earning since its foundation, and coupled with market volatility from major geopolitical events during the year.

The monetary amounts for complaints filed during 2016 ranged from as low as $10 to as much as $57,199.00, and the total amount of compensation that was paid out was $157,326.00 from a total of 165 complaints filed.

Overview of 2016 Complaints Statistics:

Total Complaints filed 165 (100%)

Complaints filed against Members 128 (77,58%)

Complaints filed against non-Members 37 (22,42%)

165 Complainants sought a record $1,813,275.00

Total amount of compensations $157,326.00

Maximum complaint amount awarded $57,199.00

Minimum complaint amount awarded $10.00

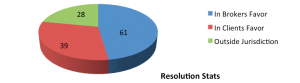

Total amount of resolutions (against Members)

Resolutions in favour of client 39 (30,47%)

Resolutions in favour of broker 61 (47,66%)

Out of jurisdiction 28 (24,87%)

Types of Complaints

Trading complaints are directly related to the process of trading on the market and the affect of execution of orders, payment of margins, calculation of commissions, forced liquidation of positions and other parts of the trade cycle. These complaints are considered by the Dispute Resolution Committee and included in the statistics.

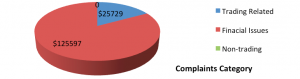

Total amount of trading complaints 57:

against Members 54

against non-Members 3

Financial complaints are related to transactions on the account, and in majority of cases involve delays in withdrawals. Such complaints do not fall under dispute resolution process; however, the Financial Commission never rejects such complaints and helps advocate the payment process with clients till the end. We do not record cases of non-payment of funds to the clients by Member-companies. Nevertheless, in cases when such complaints are received against non-member companies providing of a refund to the client from the broker is often very problematic.

Total amount of financial complaints 56:

against Members 54

against Non-Members 17

Non-trading complaints are often clients’ complaints about the facts of losses incurred as a result of cooperation with the administering traders and sales consultants. To a lesser extent these are complaints for automatic copying transactions systems and signaling services. Such complaints do not fall under the dispute resolution process; however, we always analyze the contract, risks warning, correspondence and negotiations with the client and also give our assessment of the situation and recommendations for a possible settlement of the dispute.

Total amount of non-trading complaints 52:

against Members 36

against Non-Members 16

Event Participations and Important Meetings in 2016

Financial Commission was one of the exhibitors at the 2016 iFX Expo in Hong Kong which took place at the end of January, followed by the 2016 iFX Expo in Cyprus in May. The main focus of these events were recent developments within the online trading industry including challenges, opportunities and ongoing trends discussed among market participants.

Financial Commission’s stand was in a very prominent location during the Cyprus event and benefitted from the increased exposure to the event’s industry delegates. The collective feedback that Financial Commission received during these events from industry media resources, attendees, and fund managers was highly supportive. Chairman Peter Tatarnikov had an opportunity to give a few interviews during the Cyprus event including to local TV channels as well as to Internet media resources for the financial industry.

After participating at the Cyprus conference, on July 22nd, 2016, in Minsk, Belarus, Financial Commission signed a Memorandum of Understanding (MoU) with the Association of Financial Market Development (ARFIN). The MoU provides a basis to develop favourable conditions to support the Foreign Exchange market for ARFIN members and was signed during a meeting between Financial Commission Chairman, Peter Tatarnikov, ARFIN Chairman, Alexey Sidorov and representatives of the National Bank of the Republic of Belarus. The MoU will enable cooperation to improve the dispute resolution process in Belarus, and the exchange of information between both organizations.

On October 12th, 2016 Peter Tatarnikov, Chairman of the Financial Commission (FinaCom PLC) took part in the press lunch dated for discussion of the bill on forex market regulation in Kiev, Ukraine. During the event such topics as lack of the legislation regulating forex market in Ukraine, vulnerability of private investors, the most effective approaches to forex market regulation and the liability of Ukraine towards investors were discussed.

Participants of the event announced their visions of the forex market and regulatory challenges on the territory of Ukraine, while sharing their international experience, answering journalists’ questions and providing several examples of forex regulation in Western countries.

The U.S. Commodity Futures Trading Commission (CFTC) today issued an Order filing and settling charges against J.P. Morgan Securities LLC (JPMS), a Delaware corporation headquartered in New York City, for failing to diligently supervise its officers’, employees’, and agents’ processing of exchange and clearing fees it charged customers for trading and clearing Chicago Mercantile Exchange, Inc. (CME) products and products from certain other exchanges during 2010 to 2014. JPMS is registered with the CFTC as a Futures Commission Merchant and a swap dealer.

The CFTC Order requires JPMS to pay a $900,000 civil monetary penalty and cease and desist from violating the CFTC regulation governing diligent supervision.

The CFTC Order explains that customer transactions executed on exchanges are subject to payment of exchange and clearing fees that are applied to each transaction in the normal course of business. Clearing firms such as JPMS receive invoices for these fees from the exchange clearinghouses, which the firms pass on to their customers, the CFTC Order states.

Here, the CFTC Order finds that JPMS failed to implement and maintain adequate systems for reconciling invoices from exchange clearinghouses with the amounts of fees actually charged to its customers. JPMS’ fee reconciliation process was largely manual and carried out by only one employee at the end of the month using three different JPMS systems. In addition to insufficient staff to complete the fee reconciliation process accurately, JPMS did not have adequate written policies and procedures in place regarding its clearing and exchange fee reconciliations. According to the CFTC Order, this led to instances in which JPMS overcharged some customers in an aggregate amount of approximately $7.8 million. The CFTC Order finds that JPMS discovered the problem in 2014, self-reported it to the CFTC, and thereafter took remedial steps, including refunding adversely affected customers.

The Order recognizes JPMS’ significant cooperation with the CFTC’s Division of Enforcement during the investigation of this matter.

Third Such Action Brought by the CFTC

This is the third action that the CFTC has brought over a clearing firm’s supervisory failures over fee processing:

• In August 2016, the CFTC ordered Barclays Capital, Inc. to pay an $800,000 penalty relating to its processing of futures exchange and clearing fees charged to customers (see CFTC Order and Press Release 7419-16, August 4, 2016); and,

• In August 2014, the CFTC ordered Merrill Lynch, Pierce, Fenner & Smith Incorporated to pay a $1.2 million penalty relating to is processing of futures exchange and clearing fees charged to customers (see CFTC Order and Press Release 6984-14, August 26, 2014).

The CFTC Division of Enforcement staff members responsible for this case are Susan Gradman, Joseph Patrick, Elizabeth Pendleton, Brigitte Weyls, Scott Williamson, and Rosemary Hollinger.

The Australian Securities and Investments Commission (ASIC) is warning its Registry customers to be vigilant of scam emails purporting to be from ASIC.

We are aware some customers have received emails containing attachments or links to fake invoices. Fake emails may look different to ASIC emails and generally instruct the recipient to click a link to make a payment or download an invoice.

Scammers also use viruses, spyware or malware programs to access or steal your personal information.

ASIC Commissioner John Price said, ‘Scam emails often appear at busy times of the year such as holiday and tax time, when it’s easy to overlook something suspicious.’

To help protect yourself online, some tips to keep in mind are:

keep your anti-virus, malware and spyware protection software current;

ensure you have a firewall and it is up-to-date; and

scan email attachments with security software before opening them, especially if they are executable (.exe) files or zip (.zip) files. These files are more likely to contain malware or ransomware viruses.

If you are in doubt about the authenticity of an email that you receive from ASIC, you can phone us to verify on 1300 300 630 on weekdays from 8.30am to 6.00pm (local time in your state).

ASIC’s MoneySmart website has more tips about protecting yourself from online scams at moneysmart.gov.au/scams

Following an ASIC investigation, Mr Shun Yuen Ken Li (also known as Leo Lee), of Roseville Chase, New South Wales has pleaded guilty in the Downing Centre Local Court on two charges of dishonestly using his position as an employee.

Mr Li, 37, is accused of using his position as an employee of GAIN Capital Australia Pty Ltd (GAIN Capital) contrary to Section 184(2)(a) of the Corporations Act 2001. The charges relate to orders placed by Mr Li to gain an advantage for two clients.

GAIN Capital offered clients the opportunity to trade share price index (SPI) contracts for difference (CFDs) at the ‘market-on-open’ price, i.e. a price corresponding with the price at which SPI matched during the opening auction at 9:50am.

ASIC alleges that:

between 9 April 2015 and 19 June 2015, Mr Li used his position as an employee of GAIN Capital to manually enter 13 profitable Market-on-Open Orders in SPI CFDs on the account of another person, with the intention of gaining a financial advantage for that person, and

between 26 May 2015 and 10 July 2015, Mr Li used his position as an employee of GAIN Capital to manually enter 38 profitable Market-on-Open Orders in SPI CFDs on the account of another person, with the intention of gaining a financial advantage for that person.

A pre-sentence report was ordered and the matter was adjourned to 14 February 2017 for sentence.

ASIC acknowledges GAIN Capital’s full cooperation and assistance in this matter.

The Commonwealth Director of Public Prosecutions is prosecuting this matter.

Background

Each of the charges laid under s184(2)(a) of the Corporations Act 2001carries a maximum penalty of $340,000 or imprisonment for 5 years, or both.

HSBC, JP Morgan and Crédit Agricole have been slapped with a €485million (£413million) fine by the European Commission for their role in a cartel which conspired to rig a key bank lending mechanism.

After a five-year investigation, the EU’s anti-trust watchdog said the three banks colluded to manipulate the Euribor interest rate between September 2005 and May 2008 by exchanging sensitive information ‘to distort the normal course of pricing’.

JP Morgan was given the biggest fine at €337million. HSBC was handed a €33million penalty and Crédit Agricole was given €114million. The fines were based on the time each participated in the cartel and the value of products involved.

In a statement, the European Commission said: ‘The participating traders of the banks were in regular contact through corporate chat-rooms or instant messaging services. ‘The traders’ aim was to distort the normal course of pricing components for euro interest rate derivatives.

‘They did this by telling each other their desired or intended EURIBOR submissions and by exchanging sensitive information on their trading positions or on their trading or pricing strategies.’

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies. However you may visit Cookie Settings to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Jayaprakash Jagateesan, CEO, RHT Compliance Solutions comments, “The timing of this partnership is ideal. The Government in Singapore is encouraging firms to embrace technology and go digital. Financial Institutions are looking to automate processes wherever possible and Muinmos’ RegTech products are ideally placed to help the compliance function to become more streamlined and efficient. We are excited to bring this technology to our clients.”

Jayaprakash Jagateesan, CEO, RHT Compliance Solutions comments, “The timing of this partnership is ideal. The Government in Singapore is encouraging firms to embrace technology and go digital. Financial Institutions are looking to automate processes wherever possible and Muinmos’ RegTech products are ideally placed to help the compliance function to become more streamlined and efficient. We are excited to bring this technology to our clients.”