Brexit – The full effect on the financial industry: A comprehensive and detailed report from within

This report, which was compiled by and represents research conducted by Kier Yorke, Director of Financial Sales Services at SinusIridum, looks at the effects on the entire financial sectors across Europe, with detailed figures, covering topics ranging from regulation, to financial stability, to the companies and nations that will be most, and least affected, as well […]

This report, which was compiled by and represents research conducted by Kier Yorke, Director of Financial Sales Services at SinusIridum, looks at the effects on the entire financial sectors across Europe, with detailed figures, covering topics ranging from regulation, to financial stability, to the companies and nations that will be most, and least affected, as well as what to bear in mind when doing business pre and post Brexit.

A UK vote to leave the EU would trigger a snap recession, prompt a fall in share prices and house prices and knock as much as 2% off GDP. If the UK votes to leave the EU, it is likely to entail an immediate and simultaneous economic and financial shock for the UK. We can expect a drop in business investment, hiring and confidence. A sudden stop of capital flowing into the UK could make the large current account deficit difficult to sustain and lead to a sharp fall in sterling.

For the majority of businesses in Britain the possibility the UK might leave the European Union – Brexit – is a major source of concern. Both the break with the EU and the uncertainty

associated with it would be bad for business and damaging to the UK economy. A great deal has now been written on the economic consequences for the UK of Brexit. Some of this is impartial; much of it is partisan. Very little has been written on the consequences for the rest of the EU.

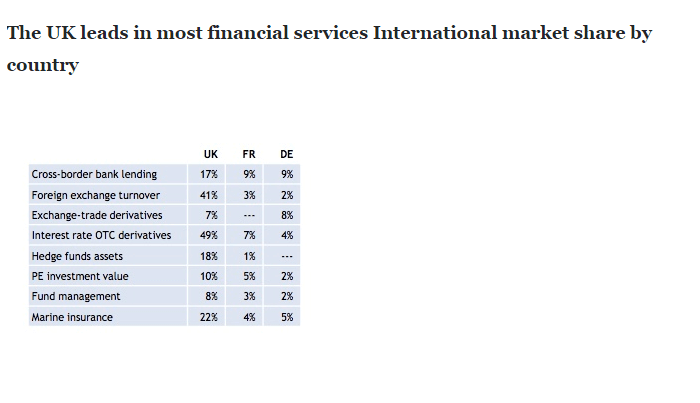

Let’s be absolutely clear, there is little prospect of London being dislodged as Europe’s leading international financial centre. This is sustained by inherent advantages and a large network of financial and professional services that are hard to replicate. However, existing EU regulations would make it harder for London to serve European markets, particularly (but not only) for retail banking and euro trading. Some business would be likely to move to Eurozone financial centres or be lost to Europe.

Competition to take this business would be wasteful. While one or two centres may ultimately benefit, businesses and households across the EU would bear the cost in terms of higher charges and poorer products.

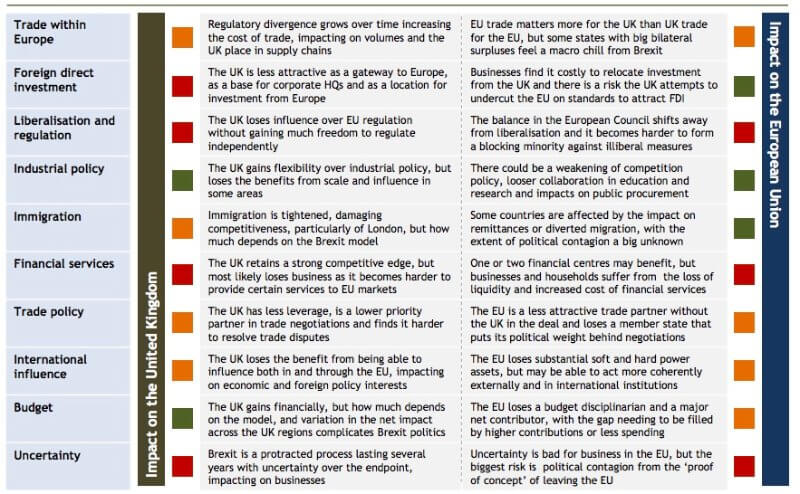

Brexit would impact on the position of both the UK and the EU in the world. In economic terms this would be most evident in trade policy. While the UK would likely be free to strike new trade deals based on domestic priorities it would have less leverage and be a lower priority than the EU for other countries. The UK would also face the huge challenge of renegotiating the existing EU deals that would no longer apply.

The EU would likewise be a less attractive partner at a time when it is only second priority for the US and Japan and a lower priority for many emerging countries. The EU may, however, be able to take a tougher stance in negotiations without the UK and make more active use of trade remedies. In addition, the EU would lose substantial hard and soft power assets although Brexit could lead to greater EU political integration and more coherent external representation in institutions and on external policy.

There are three broader ways in which the UK and the rest of the EU would be affected by Brexit, which are not captured by macroeconomic models. The first channel is uncertainty. Surveys find many UK businesses are already worried about the impact of referendum uncertainty. Yet the process beyond a referendum – if the UK votes to leave – to the point of exit and then the establishment of a new stable relationship with the EU would itself be prolonged and highly uncertain. Sterling will take a massive hit.

The second way is through the political dynamic between large states in an EU without the UK. The UK’s influence in the EU has been damaged both by the ambivalence of the UK government to the EU and by being outside the Eurozone. Even so, the UK remains one of the most influential member states. Brexit would change the relationship between other large states including, most importantly, France and Germany. It could bind them together; it could cement France’s position behind Germany in terms of influence; or it could push them apart, with the UK no longer providing political cover to mask their differences.

The third way is through political contagion. Some of the tensions in the UK regarding the EU also exist in other states, even if they manifest themselves differently and to different extents. If the UK leaves, adopts a more independent policy in sensitive areas, and is seen to succeed, this could have far-reaching political ramifications for the rest of Europe. The ‘proof of concept’ of leaving the EU could liberate disintegrative, centrifugal forces elsewhere.

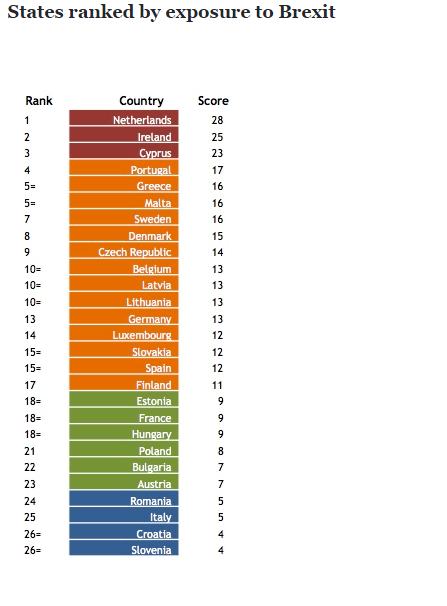

Countries like the Netherlands, Cyprus and Ireland would be hugely exposed. Each has very strong trade, investment and financial links with the UK and in the cases of the Netherlands and Ireland are closely aligned in policy terms.

Among the larger member states Germany would be affected through several channels, but perhaps most profoundly by the loss of the UK as a counterweight to France in policy debates. France may welcome the absence of the UK in policy debates, but like Spain has substantial direct investments in the UK. Italy is less directly exposed to Brexit, while Poland’s interests are concentrated on the impact Brexit would have on the EU budget and the large number of Polish residents in the UK.

All member states would, however, regret the loss of international influence enjoyed by the EU without the UK and the damage that Brexit would do to the esteem of the EU globally.

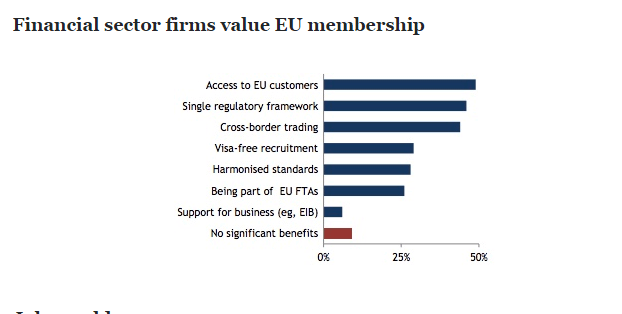

What concerns me the most is the impact of Brexit on Financial Services. Established advantages and agglomeration effects mean the UK has a strong competitive edge that would be hard to dislodge. However, existing EU regulations would make it harder for London to serve European markets, particularly for retail products and in euro trading. Business could move.

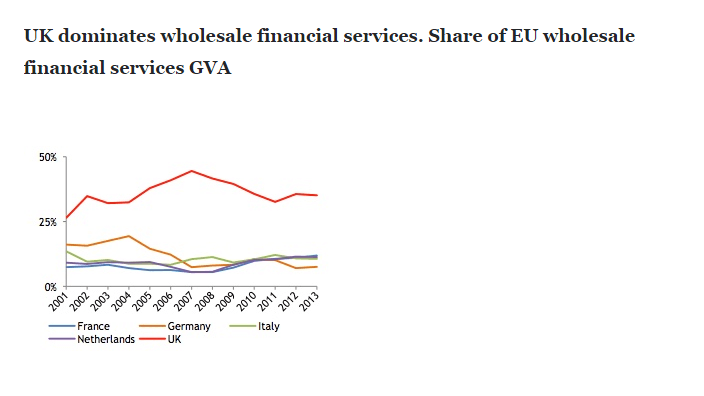

Under the Swiss or FTA models the UK must negotiate access to EU markets in financial services. The EU only allows access to countries with equivalent regulations. The approach currently varies across directives. No access is allowed in some areas, such as UCITS (undertakings for collective investment in transferable securities). The logic is that retail consumers need additional protection. By contrast, the EU takes a flexible approach to wholesale banking, where equivalence is defined largely by reference to international standards. This matters for the UK given its dominance in wholesale banking. In many other directives the EU takes an intermediate approach.

For example, the EU evaluates the equivalence of insurance regulation ‘line-by-line’ under Solvency II, although the impact is softened by transitional arrangements.

The Swiss experience highlights the risks to the UK. They have equivalence under AIFMD, are being assessed under Solvency II and will try under MIFID. But they have failed under EMIR, ostensibly due to capital requirements, but with a suspicion that the real problem is Swiss immigration policy.

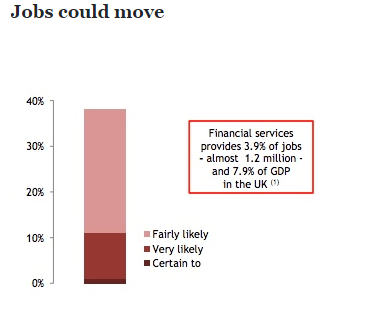

The UK is the leader in euro-denominated wholesale banking, but Eurozone countries and institutions want this activity to move to the Eurozone and be overseen by the ECB. This would be much more likely following Brexit, as the UK would no longer be protected by ECJ enforcement of single market rules. The UK might also suffer an opportunity cost from being absent from future liberalising initiatives such as Capital Markets Union, which could open up new markets in areas such as securitisation and covered bonds. The impact in the UK would be felt beyond London in financial centres such as Edinburgh, Leeds and Glasgow, as well as in the Crown dependencies.

Brexit may impact on the location, liquidity and cost of financial services in Europe if it undermines London’s competitive position. This would be costly for businesses and households across Europe. Most large European banks have major operations in London which would be costly to relocate. Only a small number of financial centres elsewhere may benefit.

The UK is highly integrated into the European financial system. Total UK claims on the EU15 alone are $880bn with most of the credit to households and firms, but some also to governments and interbank lending. European bank exposure to the UK is even greater at $1.7tn in total. It would be costly for European banks to relocate wholesale banking activity away from London.

London is not just a European financial centre – it is an international centre with a dominant position in many product areas. However, London’s international position could be damaged if large amounts of European business migrate following Brexit. There is a risk that some business, particularly more mobile activity such as derivatives, may leave Europe altogether.

The most likely beneficiaries in the EU are Paris, Frankfurt, Amsterdam and Dublin. But they cannot replicate overnight the advantages of the London ‘ecosystem’ supporting financial services, including skilled staff, legal services and market infrastructure. Competition between them borne out of new barriers to trade with London would be disruptive and costly. Businesses in Europe would lose due to higher charges, poorer products and less liquidity.

European corporates would, for example, find it more inconvenient and costly to raise capital in London, which currently provides a one-stop shop.

Brexit would likely change the balance of financial regulatory debates in Europe. The UK now takes a more interventionist and risk-averse approach to regulation. Even so, the UK largely avoids politically-motivated interventions. Initiatives such as the Financial Transactions Tax and the cap on banker bonuses would have found an easier passage in an EU without the UK.

Who is most exposed?

Brexit will impact on member states through some channels, such as international influence, to a largely uniform extent. For others the impact will vary depending on connectedness with the UK, alignment with UK policy objectives, or underlying vulnerability to shocks. The extent of exposure is revealing not only about the risks to member states, but also how much they have invested in keeping the UK in the EU.

Three countries stand out for having the highest exposure – the Netherlands, Ireland and Cyprus. Ireland is no surprise, given its proximity to the UK. The Netherlands and Cyprus, like Ireland, share very strong trade, investment and financial links with the UK. These countries also tend to be closely aligned with the UK in terms of regulatory and trade policy objectives.

Several countries have a significant exposure including Germany, Belgium and Sweden. Germany is in the middle of the pack across most metrics, suggesting Berlin will not only be influential, but also a good gauge of the wider EU interest in preventing Brexit. Sweden is particularly vulnerable due to a close policy alignment with the UK, while Belgium has close trade links.

France and Poland are among a group of countries that are more exposed to Brexit in specific areas. In the case of France midlevel trade, investment and financial linkages are balanced by often conflicting policy objectives with the UK. Poland is most exposed through migration and the EU budget.

Italy is among a small group of states in the south-east of the EU with little direct exposure to Brexit. This reflects their distance and different political cultures, which means there is less alignment of policy interests. Italy in particular may be indirectly affected by the impact of Brexit on political dynamics in the EU.

Exposures of selected member states:

The 3 main Member States most at risk of the UK’s exit of the EU

Netherlands

Dutch firms have direct investments worth €177bn in the UK, earning over €9bn in 2013, equivalent to almost 1.5% of Dutch GDP. Unilever has headquarters in Rotterdam and London. Royal Dutch Shell is headquartered in the Hague, but incorporated in the UK. Philipps has manufacturing, sales and research operations in the UK.

The Netherlands exported €42bn in goods and €7bn in services in 2013, running a surplus of €6.8bn. It has among the most intensive financial sector links to the UK with bank loans from Britain totalling €236bn in 2014. Major Dutch banks such as ING have substantial operations in the UK. While Amsterdam may take business from London following Brexit, the disruption to Dutch banks and businesses would be substantial.

The Netherlands is closely aligned with the UK in many EU policy debates. Both favour less regulation, more liberal markets, and opening up external trade. They have, for example, collaborated closely on the better regulation agenda, with the UK promoting the Dutch model in the face of French, Italian and Spanish resistance.

The Netherlands is vulnerable to the potential political consequences of Brexit. Dissatisfaction with the EU has been growing with just over a quarter of the population viewing the EU negatively. The strongly eurosceptic PVV may seek to capitalise on the political fallout from Brexit. The party won over 15% of the vote in the 2010 parliamentary elections, although it’s support fell back to 10% in 2012.

Ireland

Ireland is the only member state to share a land border with the UK and is the most deeply integrated with the UK in terms of trade, supply chains, migration, language and culture. Ireland exported €14.8bn of goods and €5.8bn of services to the UK in 2013, the equivalent of almost 12% of GDP and substantially higher than any other member state. However, Ireland was one of only seven countries to run a trade deficit with the UK, importing €22.3bn in goods and €9.1bn in services.

The investment relationship is both broad and deep, with Irish firms having over €13bn invested in the UK, earning over €800m in 2013, equivalent to almost 0.5% of GDP. Irish investment in the UK is, however, small compared to UK investment in Ireland, which stood at €51.2bn in 2013 or the equivalent of nearly 30% of Irish GDP.

Financial links are strong, with a history of banks operating in both countries, including Ulster Bank, which has 111 branches in the Republic of Ireland. Several international banks have Dublin operations that are closely integrated with London. Similarly, many hedge and private equity funds operate out of Dublin but with close links to the UK. Brexit would create costs, but also opportunities for these firms to take business from London.

The number of Irish nationals living in the UK is estimated at 329,000, second only to Poland among EU member states, but much larger as a share of the Irish population. The UK and Ireland share similar approaches to economic policy, making them instinctive collaborators.

Cyprus

Cyprus is small and geographically remote from the UK, but closely linked due to a number of historical and cultural factors, making Cyprus one of the member states most exposed to Brexit. Cyprus exported €1.3bn to the UK in 2013, over 7% of GDP, although Cyprus ran a small trade deficit and, unusually, the vast majority of Cypriot exports were in services.

This in turn reflects the extensive financial sector links between the two countries, with many of the larger Cypriot banks maintaining substantial operations and taking deposits in the UK. UK-based banks have borrowed in total the equivalent of over 40% of Cypriot GDP and lent to entities in Cyprus an amount equal to more than 30% of GDP.

The UK-Cypriot relationship is unusual among EU states in many regards. Cyprus is a member of the Commonwealth, was a British colony until 1960 and is still today the home for two sovereign British military bases. People-to-people links remain strong, with over one million British visitors to Cyprus each year and 34,000 Cypriot nationals and as many as 300,000 people of Cypriot descent living in the UK, equivalent to over one third of the current population of Cyprus.

38% of Cypriot’s view the EU negatively, largely a legacy of Cyprus’ economic crisis and bail-out programme. Cyprus’ strong links to not just the UK, but Greece, make the country very exposed to the potential contagion effects of Brexit.

Conclusions

A referendum on Brexit is now certain. While the outcome is far from a foregone conclusion, a vote for Britain to leave the EU is very possible.

The impact of Brexit on British businesses, the UK economy and wider British interests would be severe and felt across multiple channels. Both the path and the endpoint, in terms of the new relationship between the UK and the rest of the EU, would be uncertain, compounding the costs to the UK.

The direct impact on the rest of the EU would also be significant. The export, supply chain, investment and policy interests of many large corporates would be adversely affected, but perhaps the single biggest impact will be on the cost of raising finance in Europe which is likely to increase.

Brexit would have a wider political impact on the EU, both by disrupting internal political dynamics and because of the risk of political contagion if the ‘proof of concept’ of leaving the EU encourages disintegrative forces in other member states.

Europe would also lose esteem and influence around the world. Member states would be affected in different ways and to different extents. This will most likely influence ways in which states are willing to engage and accommodate the UK during the pre referendum negotiation.

All member states would, however, feel the impact of Brexit, both politically and economically.