Time for FX brokerages to start considering new types of payment processors? The regulators may turn on the existing ones

The time has come to innovate and evolve the way payments are processed to online brokerages. We examine why this is, in great detail.

As the FX industry relies completely on electronic, online and hosted services for the operation of every component of its business from the actual trading platform itself, to accessibility to live market pricing via aggregated price feeds electronically provided by prime brokerages, to the relationships with Tier 1 banks, market infrastructure such as connectivity and lastly, payment channels, should one particular component no longer become available, substantial collateral damage would occur.

FinanceFeeds considers the online payments industry to be a completely separate entity, operated by completely separate executives with completely separate career paths and business ethos to the established retail and institutional electronic trading industry, however there is one specific matter that should perhaps be considered, that being the almost over-reliance on a handful of payment processing providers which have angled their business intentionally toward the FX (and binary options) sectors.

Whether receiving direct payments from retail customers, processing withdrawals to client bank accounts, or operating an omnibus account on behalf of large white label partners or introducing brokers, a few payment processing providers are in widespread use, largely due to their ability to conduct payment transfers effectively from all regions of the world, circumnavigate risk related ‘red flags’ that are part of MasterCard or Visa’s commercial remit, that being not to enable transfers from countries with high levels of fraudulent activity such as money laundering, and not to facilitate payments to websites that actively solicit for nefarious goods or services such as lottery or mail fraud, and not to provide payment channels to countries in which certain activities are blocked.

For example, binary options on an OTC basis is not legal in the United States, yet FinanceFeeds has conducted substantial research and can confirm that a vast amount of brands and their respective market makers in the binary options business, which is under massive fire from regulators and governments around the world due to its largely completely fraudulent nature, are still actively soliciting clients in the US and stealing money from them with very little recourse, because the payments are being processed via firms that ‘scramble’ the origin and business activity of the firm which is receiving the payment by processing via third party providers and effectively laundering the money via holding accounts in order that it does not show up on the red flag list of Visa or MasterCard.

Last year, PacNet, which operates the brand Counting House, is a large payment processing provider which has a significant number of commercial customers in the retail FX industry, as well as electronic entertainment and gaming sectors.

According to legal notes from the US Department of the Treasury’s Office of Foreign Assets Control (OFAC), the US government’s sanctions on Counting House and PacNet are have been applied in order to target what the officials have termed a significant transactional criminal organization whch launders millions in illicit funds worldwide.

PacNet, the US government states, has a lengthy history of money laundering by knowingly processing payments on behalf of a wide range of mail fraud schemes that target victims in the United States and throughout the world. PacNet is the seventh TCO targeted under transactional criminal organization laws.

With operations in Canada, Ireland, and the United Kingdom, and subsidiaries or affiliates in 15 other countries, PacNet is the third-party payment processor of choice for perpetrators of a wide range of mail fraud schemes.

U.S. consumers receive tens of thousands of fraudulent lottery and other mail fraud solicitations nearly every day that contain misrepresentations designed to victimize the elderly or otherwise vulnerable individuals. PacNet has a nearly 20-year history of knowingly processing payments relating to these fraudulent solicitation schemes (recently binary options), which result in the loss of millions of dollars to U.S. consumers.

PacNet’s processing operations help to obscure the nature and prevent the detection of such fraudulent schemes. In a typical scenario, scammers will mail fraudulent solicitations to victims and then arrange to have victims’ payments (both checks and cash) sent directly or through a partner company to PacNet’s processing operations.

This is how Israeli OTC binary options firms manage to solicit and extract funds from US customers, even though that is an illegal activity in the US.

Victims’ money, minus PacNet’s fees and commission, are made available to the scammers through wire transfers from the PacNet holding account and by PacNet making payments on behalf of the scammers, thereby obscuring the link to the scammers. This process aims to minimize the chance that financial institutions will detect the scammers and determine their activity to be suspicious.

In 2002, as part of a forfeiture action in the U.S. District Court for the Western District of Washington, two of PacNet’s major corporate entities in Canada and Ireland acknowledged that the use of the mail to market lottery chances, shares, and interests within the United States, as well as the use of facilities of interstate or foreign commerce within the United States to handle payments for these types of fraudulent solicitations, violate U.S. federal statutes.

One of the travesties of this is that Counting House angles itself as a major supplier of payment processing services to FX and OTC binary options firms, and in times at which it is difficult to obtain merchant services from many providers, firms could inadvertently use this company.

This represents another potential pitfall that brokers should be aware of, in a similar vein to our research which deduced that Tier 1 banks in top quality jurisdictions including US, Canada, Britain, Australia, Israel and Cyprus – effectively all regions with a high level banking environment (and in which Counting House operated), good safety and compliance rulings and large institutions that carry corporate accounts for some of the world’s largest blue chip companies as well as being home to the lion’s share of the world’s retail FX industry – are continuing to curtail their service and are increasingly turning away FX brokerages as customers.

This means that not only do brokers have limited options as to where to store their operating capital and client funds, but also are now becoming the target of thefts from corporate bank accounts because FX brokers are being increasingly forced to use third degree banks in less than salubrious regions, which, according to our research, is causing great difficulties in security of funds.

One of the criminal activities listed by the US Department of Treasury relating to Counting House’s structure was the use of a ‘third party’ account which allows funds to be deposited into what appears to be a legitimate entity, it is then ‘cleaned’ and sent to the requesting company.

Many companies facilitating this type of service use the same type of structure. Some call themselves ‘algorithmic payment processors’ alluding to the use of some type of algorithm which attempts all types of channels to process a payment that otherwise may not be allowed by a government or a merchant services provider, until a gateway accepts it.

This is absolutely not how these systems work. There is no algorithm, it is purely sold as that to make it appear as though it is a technological solution and part of the ‘FinTech’ structure that powers the world’s financial markets economy, when actually that is a deflection of attention from the real nature of the business which is, if the US Department of Treasury’s decision is to be taken as a benchmark, tantamount to money laundering.

Any activity that seeks to deflect funds from an originating source (retail customer, white label partner or IB) and then deposit the funds to a third party account in a different name to where it is intended, then reprocess it to the requester is a form of money laundering, as it ‘cleans’ the identity of the money and therefore circumnavigates any restrictions on that type of business activity put in place by either governments or Visa or MasterCard.

Israel’s national airline EL AL onboarded SafeCharge’s solution recently, largely because of its ‘smart routing’ capabilities and its ability to acilitate the acquiring relationship with multiple third parties giving EL AL access to global acquiring services and the utilisation of multiple APMs.

What does that mean? Perhaps smart routing refers to the use of third party accounts to ‘clean’ the money that would otherwise be refused by merchant services providers.

As long ago as 2014, the US Department of Justice initiated an investigation called “Operation Choke Point” which instigated criminal and civil litigation against 15 banks for using payment processing compamies that move money for various suspect businesses.

According to documents released on in May 2014 by the House of Representatives’ Oversight Committee, the DOJ had criminal probes open of four payment processors, one bank and several officials as of November 2013.

The department had separate investigations into at least 10 banks and payment processors under a civil fraud law, according to a memo from a DOJ official that was included in the documents.

Maame Ewusi-Mensah Frimpong, an official in the DOJ’s civil division, wrote in the memo that the probe had already caused some banks to stop processing payments for entities the firms believed could be involved in fraud against consumers.

“We believe we already have denied fraudulent merchants access to tens, if not hundreds, of millions of dollars from consumers’ bank accounts, and that amount will increase daily and indefinitely,” said Mr Frimpong.

This occurred at around the same time that the CFTC and NFA banned credit card deposits to FX brokerages or other online trading entities by retail customers, the only method being direct bank transfer, and receipt of withdrawal request by bank transfer.

Outside of the payment processors’ ability to dress up their services as FinTech solutions by using characterized buzzwords such as ‘algo’ or ‘instant’, these methods are often referred to as ‘Card Schemes’, thus carry negative connotations.

Card schemes by their definition are payment networks linked to payment cards, such as debit or credit cards, of which a bank or any other eligible financial institution can become a member. By becoming a member of the scheme, the member then gets the possibility to issue or acquire cards operating on the network of that card scheme.

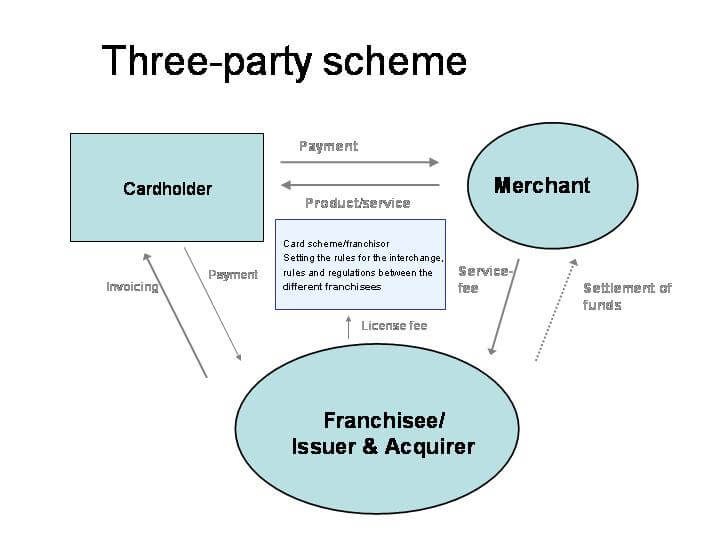

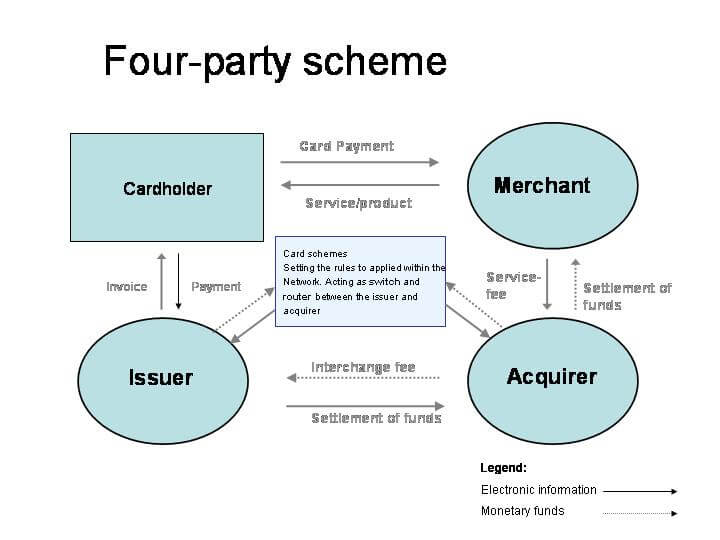

There are generally two categories, one involving three parties and another involving four parties. A three-party scheme consists of three main parties as described in the diagram here.

In this model, the issuer (having the relationship with the cardholder) and the acquirer (having the relationship with the Merchant) is the same entity. This means that there is no need for any charges between the issuer and the acquirer. Since it is a franchise setup, there is only one franchisee in each market, which is the incentive in this model. There is no competition within the brand; rather you compete with other brands.

Examples of this setup are Diners Club, Discover Card, American Express, although in recent times these schemes have also partnered with other issuers and acquirers in order to boost their circulation and acceptance.

In a four-party card scheme, the issuer and acquirer are different entities, and this type of scheme is open for other institutions to join and issue their own cards. This signifies card schemes such as Visa, MasterCard, Verve Card, UnionPay and RuPay. There is no limitations as to who may join the scheme, as long as the requirements of the scheme are met.

When taking this into consideration, despite the Financial Conduct Authority (FCA) having astonishingly upheld PacNet as a regulated payments processor one day after it was sanctioned by the US government, it may well be the time to begin future-proofing the payment channel by looking away from these types of firms and seeking new channels as regulators may begin to chop these services.

In a meeting with Saxo Bank senior executives in London at the end of last year, FinanceFeeds discussed the possibilities that brokerages may begin expanding their own payment processing services and banking systems to suit the FX industry and offer a bona fide alternative. This would be a welcome direction indeed.

The industry is, after all, far more sophisticated and evolved at retail level than it was ten years ago, hence it is only a matter of time before the hawk-eyed regulators put a stop to the use of PacNet-style payment processing companies altogether, hence now’s the time to start working on institutional-grade alternatives.