FXCM and CEO Drew Niv banned from US: Full details of FXCM’s several years of trading against customers

FXCM always told customers that they traded on FXCM’s no dealing desk platform, however the firm had an undisclosed interest in market maker that consistently ‘won’ FXCM trading volume and was therefore taking the opposite positions FXCM’s retail customers

Yesterday, in an extraordinary bombshell, the Commodity Futures Trading Commission (CFTC) took the decision to ban North American electronic trading giant FXCM and its CEO Drew Niv from operating in the US market.

In its court filings and order instituting proceedings with regard to the Commodity Exchange Act imposing remedial sanctions, the CFTC has reason to believe that Dror (Drew) Niv and William Ahdout have violated the Commodity Exchange Act and the CFTC regulations to which both respondants have submitted an offer of settlement.

Trading against customers, whilst all the while maintaining that the firm used a no dealing desk model

Trading against customers, whilst all the while maintaining that the firm used a no dealing desk model

From September 4, 2009 through at least 2014, FXCM and FXCM Holdings, by and through their officers, employees, and agents, including Respondents Niv and Ahdout, engaged in false and misleading solicitations of FXCM’ s retail foreign exchange customers.

FXCM represented to its retail customers that when they traded forex on FXCM’s “No Dealing Desk” platform, FXCM would have no conflict of interest. According to these representations, retail customers’ profits or losses would be irrelevant to FXCM’s bottom line, because FXCM’s role in the customers’ trades was merely as a credit intermediary. According to FXCM, the risk would be borne by banks and other independent “market makers” that provided liquidity to the platform.

Contrary to these representations, FXCM had an undisclosed interest in the market maker that consistently “won” the largest share of FXCM’ s trading volume – and thus was taking positions opposite FXCM’s retail customers. That market maker was an FXCM-backed startup firm that was founded by a former FXCM executive while he was working at FXCM, that operated for the first year of its existence out of FXCM’ s offices, and that shared most of its trading profits with FXCM.

FXCM also made false statements to NFA staff to conceal its role in the creation of its principal market maker as well as the market maker’s owner’s previous role as an FXCM executive.

Mssrs Niv and Ahdout directed and controlled FXCM’ s operations throughout the relevant period and were responsible, directly or indirectly, for violations described herein. Niv was responsible, directly or indirectly, for the false statements made to NFA.

FXCM, which was founded in 1999 and became a registered FCM in 2001, provides retail a FX trading environment and acts as counterparty in transactions with its retail customers in which customers can buy one currency and simultaneously sell another, and as of July 31, 2016, FXCM had over 20,000 active retail customer accounts representing more than $170 million in liabilities.

Until approximately 2007, FXCM provided liquidity to its retail forex customers primarily through an internal dealing desk – a division of FXCM that determined the prices offered to customers and held positions opposite customers.

In or around 2007, FXCM transitioned from utilizing a dealing desk to transact with customers to using what it termed an “agency” model for the majority of its retail forex customers, which it described to customers as providing “No Dealing Desk” forex trading. (FXCM using its dealing desk to trade with retail customers, by contrast, was referred to as the “principal” model.)

Whereas a dealing desk broker “acts as a market maker” and “may be trading against your position,” FXCM claimed that its agency model “eliminated” that “major conflict of interest” between broker and retail customer.

In FXCM’s agency model, price quotations were provided not by FXCM’s internal dealing desk but by banks and other third-party “market makers” – sometimes also referred to as “liquidity providers” or “LPs.”

FXCM explained its agency model to its customers as follows: “When our customer executes a trade on the best price quotation offered by our FX market makers, we act as a credit intermediary, or riskless principal, simultaneously entering into offsetting trades with both the customer and the FX market maker.”

FXCM claimed that trading on its agency model was different from a dealing desk broker because: “We earn trading fees and commissions by adding a markup to the price provided by the FX market makers and generate our trading revenues based on the volume of transactions, not trading profits or losses.”

FXCM Creates an Algorithmic Trading System to Trade Opposite Customers

In 2009, Niv, Ahdout, and others at FXCM formulated a plan to create an algorithmic trading system – an FXCM computer program that could make markets to FXCM’s customers and thereby either replace or compete with the independent market makers on FXCM’s No Dealing Desk platform.

Mssrs Niv and Ahdout hired a high-frequency trader to a Managing Director position at FXCM. HF Trader’s employment agreement, signed by the HFT trader and Mr Ahdout, provided that FXCM would pay the HFT Trader a base salary plus a bonus of 30 percent of trading profits generated by the HFT Trader’s algorithmic trading system, with FXCM keeping the remaining 70 percent. The HFT Trader began working for FXCM on October 5, 2009 and ultimately developed the algorithmic trading system for FXCM.

FXCM Spun Off Its Algorithmic Trading System As a New Company Owned by the high frequency trader

In early 2010, when HF Trader was finalizing his trading algorithm, FXCM’s Compliance department raised concerns that trading against FXCM retail customers might contradict FXCM’s marketing statements about its No Dealing Desk model.

FXCM determined that HF Trader would form his own company and operate as an “external” liquidity provider for FXCM. On March 23, 2010, The HFT Trader formed his new company (hereinafter, “HFT Co”). FXCM intended that HF Trader, under the auspices of HFT Co, would use his trading algorithm to trade on FXCM’s No Dealing Desk platform.

On April 14, 2010, the HFT Trader resigned from FXCM. HF Trader and FXCM agreed that HF Trader’s resignation would not change the economic relationship between FXCM and HF Trader, including, as stated in his employment contract, HF Trader’s retention of 30 percent of his algorithmic trading profits, with FXCM capturing the residual 70 percent.

To that end, a March 1, 2010 services agreement between HFT Co and FXCM, and a superseding May 1, 2010 services agreement between HFT Co and FXCM Holdings, provided that HFT Co would make monthly payments to FXCM in the amount of $21 per million dollars of trading volume executed by HFT Co. HF Trader and FXCM believed that this amount approximated 70 percent of HFT Co’s profits from trading on FXCM’s retail forex platform.

HFT Co Maintained a Close Relationship With FXCM

To help launch HFT Co’s operations, FXCM gave HFT Co a $2 million interest-free loan, and allowed HFT Co to use FXCM’s prime broker through a “prime of prime” account. When HF Trader resigned from FXCM, he continued working from FXCM’s offices, rent free. HFT Co was located in FXCM’s offices in New York City until approximately April 2011, when the company finally moved into its own office space, in Jersey City, New Jersey.

HFT Co also used the HFT Trader’s trading algorithm, which was FXCM’s intellectual property, to conduct its trading. For a period of time, HFT Co used FXCM’s servers and other technology, including FXCM’s email systems. HF Trader actively used his FXCM email address until at least September 2011, and his FXCM email account was still receiving emails in 2014.

Two FXCM employees who assisted HFT Co received supplemental bonuses from FXCM, reimbursed by HFT Co, on account of their work. One of these employees spent approximately 80 percent of the work week at HFT Co’s offices from 2011 until 2014.

FXCM Received Nearly $80 Million in Revenue from HFT Co’s Trading

Pursuant to the May 1, 2010 services agreement, FXCM sent HFT Co monthly invoices, which were to be paid by HFT Co to FXCM Holdings. Through August 2011, HFT Co. paid to FXCM Holdings $21 per million notional volume transacted by HFT Co on the FXCM retail forex platform and paid $16 per million from September 2011 through July 2014. From 2010 to 2014, no market maker besides HFT Co paid FXCM for order flow.

Notwithstanding the formal documentation of the monthly payments from HFT Co as reflecting a fixed $21 fee per “aggregated volume of Transactions executed,” in reality the payments represented HFT Co and FXCM’s agreement to share profits derived from HFT Co’s trading against FXCM’s retail customers.

FXCM viewed HFT Co’s profits and losses (“P&L”) from HFT Co’s trading as essentially belonging to FXCM, less the 30 percent HFT Co was permitted to keep. For instance, FXCM calculated its monthly preliminary P&L statement, in part, by taking HFT Co’s monthly P&L and simply subtracting 30 percent. When spreads tightened and HFT Co’s profits dropped to considerably less than $30 per million trading, FXCM and HFT Co amended the services agreement to lower the payments per million dollars.

HFT Co reported its P&L to FXCM on a weekly basis for a period of time following its formation. The invoices FXCM sent HFT Co seeking “Rebate for FX Trades” described the amounts billed as “P&L.” In exchange for these payments from HFT Co, FXCM agreed that it would favor HFT Co over other market makers in routing retail customer orders.

FXCM permitted HFT Co to win all “ties” with other market makers; provided HFT Co with a real-time view of price quotations offered by other market makers; and added smaller markups to HFT Co prices than to prices provided by other market makers.

On the day of HF Trader’s resignation from FXCM, HF Trader’s trading algorithm was used in a “full-scale trading session” for the very first time. Based on the trading that day, FXCM anticipated that HFT Co would capture approximately 25-30% of overall trade volume on FXCM’s No Dealing Desk Platform.

In addition to favoring HFT Co over other market makers, HFT Co made use of, and FXCM allowed HFT Co to use, a hold timer that enabled HFT Co to execute a trade at the start or end of a hold timer period, whichever was better for HFT Co. In late 2011 and 2012, HFT Co continued to make use of a hold timer but would accept or reject the trade based on the price at the end of the hold timer period. HFT Co also made use of a “previous quote” practice whereby HFT Co submitted a quote to FXCM and FXCM would respond with an execution request based on the trading limits contained in a customer limit order and not the previous quote provided by FXCM.

In total, through HFT Co’s monthly payments from 2010 through 2014, HFT Co rebated to FXCM approximately $77 million of the trading revenue HFT Co achieved.

FXCM Concealed Its Relationship with HFT Co from Its Customers

As of October 2010, FXCM’s website promised “No conflict of interest between broker and trader” and “No dealer intervention in trades,” stating that”every trade is executed back to back with one of the world’s premier banks or financial institutions, which compete to provide FXCM with bid and ask prices.” FXCM did not disclose that its principal market maker, HFT Co, was a startup firm spun off of FXCM.

For example, FXCM’s website implied that its market makers were institutions independent of FXCM: “We have obtained close banking relationships with some of the world’s largest and most aggressive price providers.” The website continued: “FXCM does not take a market position – eliminating a major conflict of interest. A dealing desk broker, which acts as a market maker, may be trading against your position. However, with our No Dealing Desk execution, we fill your orders from the best prices available to us from the banks.”

As another example, in 2011, FXCM published a diagram showing banks that acted as market makers for FXCM and showing the “percentage of volume to each liquidity provider”: BNP (13.5%), Citi (8.0%), Deutsche Bank (3.5%), Dresdner (13.3%), Goldman (14.4%), JP Morgan (3.6%), Morgan Stanley (8.0), and “Citi-Prime Broker (All Others)” (35.8%). HFT Co the liquidity provider with by far the largest volume – was not specifically identified but instead listed under “Citi-Prime Broker (All Others).”

“Good catch” says employee

When a list of FXCM’ s top liquidity providers for the first half of 2010 was circulated internally, showing HFT Co with over 17 percent of the company’s volume, an FXCM employee asked whether that reference should be “blacked out.” Another employee responded: “Good catch, put them as HFT 1 …. ”

In September 2011, an FXCM executive raised “Compliance Concerns” with members of FXCM’s Compliance department, noting a problem with HFT Co “hanging orders” that arose from “the fact that the [HFT Co] adapter is different technology than the rest of the bank adapters.” An FXCM compliance officer responded: “Given the sensitivity of the counter party involved we would prefer the events don’t happen so that we do not draw unwanted attention.”

FXCM did not disclose HFT Co as a market maker to the retail public until late 2012. Even then, at that time, in response to an individual posting about HFT Co on an online bulletin board called “Forex Factory,” FXCM obfuscated HFT Co’s relationship to FXCM.

The Forex Factory post, anonymously written by “fx insider,” stated: “So I just heard something interesting from a friend about FXCM’ s ‘no dealing desk’. Apparently their largest liquidity provider by far is a small firm named [HFT Co], which is owned by FXCM itself and was set up solely to act as counterparty to FXCM clients. They sit on top of FXCM’ s liquidity pool with last look so that for every FXCM trade, they can choose whether to take it or pass it on to normal liquidity providers. Can anyone confirm this? It would be interesting to know how much information is shared.”

Two days’ later, FXCM posted its response on Forex Factory, stating: “While FXCM does own a liquidity provider, the name of that company is Lucid Markets. It’s an institutional level liquidity provider in the forex market and to date had provided no liquidity to FXCM’s retail no dealing desk execution.” FXCM then implied that it was restricted from identifying HFT Co to the public as one of its market makers, stating: “Non-disclosure agreements mean that we don’t normally name the 17 liquidity providers that stream prices on our No Dealing Desk feed.” In fact, there was no non-disclosure agreement between FXCM and HFT Co, and, as noted above, FXCM had disclosed ten of its other market makers to the public.

FXCM’s response also implied that HFT Co did not, as “fx insider” put it, have a unique ability to “choose whether to take” FXCM trades, and that FXCM lacked an ownership interest in HFT Co: “While the majority of liquidity providers in this list are banks, there are also some hedge funds and other financial institutions, one of which is HFT Co. However FXCM does not own them, nor do they have control over what orders can go to other liquidity providers.” To the contrary, because HFT Co did have both real-time read of book of FXCM’s other market makers and the ability to win all ties, “fx insider” was correct in stating that HFT Co had the power to choose to take whatever trades it wished.

FXCM Made False Statements to NFA About HFT Co

In connection with NF A’s 2013 examination ofFXCM, NFA compliance staff met with FXCM executives in Chicago on October 24, 2013. In response to NF A’s questions about FXCM’s relationship with HFT Co, Niv omitted to mention any of the details described above concerning FXCM’s relationship with HFT Co and its principal, HF Trader. Instead, Niv misrepresented that he had a prior working relationship with HF Trader from when HF Trader was a trader employed by other liquidity providers.

Members ofFXCM’s Compliance department also made a series of misstatements to NFA. On October 22, 2013, two days before FXCM’s meeting with NFA, an FXCM compliance officer told NF A in an email: “FXCM LLC does not have any direct or indirect ownership, interest, or affiliation with entities that provide liquidity to retail clients.”

Given, among other things, FXCM’ s interest in HFT Co, this statement was false. After NF A sought clarification of this statement, asking FXCM to “provide representation as it relates to owners, principals, APs [associated persons], employees, and affiliates of FXCM,” another compliance officer compounded FXCM’s previous misrepresentation in a March 24, 2014 email:

“To my knowledge, there are no present or past owners, principals, APs, or employees of affiliates of FXCM LLC that have direct or indirect ownership, interest, or affiliation with entities that provide liquidity to retail clients on our No Dealing Desk Model.”

This was not true, as the compliance officer knew, because HF Trader, a former employee (and, indeed, an executive) of FXCM, was the principal and 100 percent owner of HFT Co, which was the primary provider of liquidity to retail clients on FXCM’s No Dealing Desk platform.

On April 4, 2014, in response to further attempts by NF A to clarify the relationship between FXCM and HFT Co, an FXCM compliance officer stated in an email: “The HFT trader served as a consultant for FXCM from October 2009 through April 2010. The HFT trader worked primarily on software coding.”

Once again, the compliance officer’s representation to NF A was false and misleading. HF Trader was not an FXCM “consultant” but an executive of FXCM with an employment agreement, and in light of NF A’s obvious interest in FXCM’s relationship with HFT Co it was deceptive to characterize HF Trader’s work at FXCM – i.e., creating the trading algorithm that HFT Co used to trade opposite FXCM’s customers – generically as “software coding.” Mr Niv generally participated in and approved of responses to NFA.

As a result of all of this, the settlement accepted by the CFTC has resulted in an order that FXCM must pay $7 million within ten days of the order which was set in force yesterday, and that Drew Niv and FXCM shall desist from further violating section 9a (4) of the Commodity Act.

Additionally, and perhaps more gravely, FXCM has been ordered not to accept new customer accounts following the entry of the order, on yesterday’s date and Mssrs Niv and Ahdout will within 30 days from now withdraw from registration to the CFTC in all capacities and never apply for registration again, meaning that is the end of the road for FXCM in the US market.

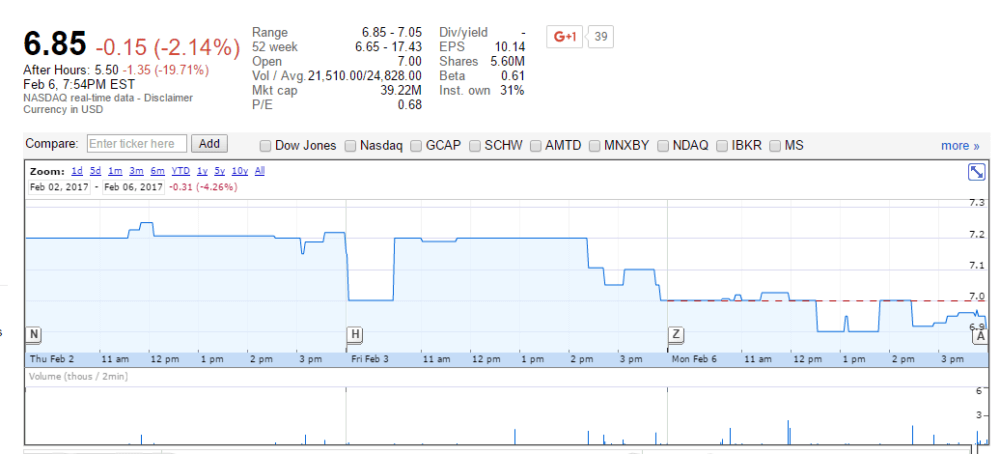

FXCM share prices collapsed this morning, and it is very likely that they will continue to do so as the company will very likely not make a recovery from this fundamental operational breach of trust over such a long period of time.

GAIN Capital will purchase the entire US client book from FXCM, making it the largest brokerage in the US by a massive margin.