“Mind The Gap!” – The life and times of a man on the move Episode 80

Prime brokerage in China? Yes! It really does exist as Western giant pips the banks once again, and when Wiki is a little less Wiki than it should be, we should all be careful!

In this weekly series, I look back on what stood out, what was bemusing, amusing and interesting during my weekly travels, interesting findings within the FX industry and interaction with an ever-shrinking big wide world. This is purely observational and for your enjoyment

XTXing the Chinese institutional market

Three years ago this week, I stood in front of over 300 executives in Shanghai from brokerages to banks, and explained that it had become clear that as the Chinese FX and OTC electronic trading market becomes more advanced, and the government begins to realize the size of the transactions that are being conducted overseas via monitoring, the entire topography would become established within Mainland China.

I said at that time that when the liquidity rush comes to the domestic market, China will dominate its own institutional and retail FX industry from within, and this has certainly become the case so far.

It is part of the ethos of the government’s communist policy that overseas banks cannot operate clearing and trading centers in Mainland China, therefore there has until now been no way that any of the OTC FX business would be able to operate solely within China without the Chinese brokers, IBs and hedge funds using an external prime brokerage – that’s assuming that they want to conduct business correctly and pass all order flow to a Tier 1 bank.

This of course meant that most domestic market Chinese retail FX brokerages were operating a pure B book, without even a price feed from a prime of prime broker, and in many cases attempting to dupe traders by putting the logos of Tier 1 banks on their marketing materials and suggesting, falsely, that order flow was going to them. I have caught a few of these pretenders out at events in the People’s Republic over the years.

Now, however, there is a breakthrough, and yet again, it is the non-bank market makers that are leading the way and paving a path into regions that the Tier 1 banks are simply unable to reach.

It was with great interest this week to learn that XTX Markets, which is now number one in the world in terms of global FX Tier 1 dealing market share, has become the first non-bank market maker to price to China’s FX interbank market, CFETS.

In what can really be described as a stroke of genius, XTX Markets has gone one further than just enter the market and offer non-bank liqudity via Electronic Communication Network, but has actually registered itself as a liquidity provider for G10 markets, with Bank of China, the first prime broker in the Chinese market, which is also owned by the government, as its prime broker.

This is the first time any non-Chinese Tier 1 dealer has managed to create a permanent relationship with a government-owned Tier 1 bank in China, and it is really a testimony to how flexible these market makers are compared to the bureaucratic single dealer platforms at banks, which are subject to all kinds of government restrictions especially when approaching communist countries.

CFETS published this week that the addition of XTX has “injected new liquidity into the market for interbank foreign currencies and further enhanced the price competitiveness of the trading centre platform”.

I should think it has! Until now, Chinese traders were stuck with either the slow-moving, government controlled Chinese stocks, which are hard to make any profit on due to the government ensuring that all stock (all companies listed on there are owned at least 30% by the Communist Party) stays non-volatile, or they could trade on local exchanges, which, as we know, are not trusted by the locals due to their unbelievable spate of b-booking despite masquerading as exchanges, a practice that put over 300 exchange executives in the South China region in jail in 2017.

As a result, hunger for global free markets, with proper movements and free market currency trading was always dominant among the big traders in China, many of whom are IBs doing over 90,000 lots per month.

Just under a decade ago, it was possible to obtain a prime brokerage agreement with a capital base of just $5 million, but now it is almost impossible with $50 million and in some cases no deal will be done unless $100 million is on the table.

This matters for two important reasons when considering unlocking the massive potential of China’s retail business.

Firstly, Britain’s large interbank dealers are weary. Their non-electronic trading divisions such as mortgage and consumer credit lending entities have been battered by financial crises in the last few years of the previous decade, and have been subject to multi-million dollar fines for misselling of payment protection insurance, have been censured for benchmark rate corruption, and have lost billions in unpaid credit during the 2008 and 2009 credit crunch, which saw most of them having to be bailed out by the taxpayer.

This has created a situation in which the main Tier 1 banks are now ultra-conservative and are still licking their wounds by selling off retail divisions in their entirety, and restricting how much risk they take on counterparty credit extension to retail brokerages.

Complexity due to lack of credit and massive capital requirements? No problem in China

Meanwhile, brokers which have to face these counterparties have to stump up massive capital bases to maintain relationships with them and still be subjected to last look order execution on single-dealer platforms and then have to strike up relationships with further non-bank electronic communications networks such as EBS, Currenex, Hotspot FX and FXall in order to attempt to provide a more comprehensive liquidity solution against the banks’ pulling the rug out from under everyone’s feet.

The same brokerages are battling with this whilst focusing on mainland China, and its own restrictions toward allowing any transaction over $50,000 (which is nothing because most brokers have an omnibus account or a prime brokerage agreement and have to send much higher figures than that each month to overseas banks of the brokers they work with) out of the country for the purposes of derivatives trading.

As of 2017, all transactions over $50,000 are subject to a client signature to document the purpose of the transfer. If it is for derivatives trading of any kind, it is no longer allowed.

Just as this happened, China’s own banks, all of which are owned by the state, are massively well capitalized and have a very clever model indeed.

They do not expose themselves to risk, and they have assets which consist of property, cash, investments in company stock and indices that are so enormous that it is hard to quantify.

These banks, unlike the weary western banks, will extend counterparty credit to FX brokerages in China without the blink of an eyelid over risk.

Western banks are already wounded enough and are restricting what they can see quite transparently. It would be futile for a Western prime broker with no presence in mainland China to go to a Western bank’s eFX desk and ask for a large prime brokerage deal because of a massive Chinese partner that has been onboarded.

There is no way for the bank to check how large and how well capitalized that firm is, as one is one side of the firewall, and the other is, well, the wrong side.

The answer would be no.

For Chinese banks, offering Chinese liquidity to Chinese prime of primes and then distributing aggregated feeds to Chinese FX brokerages, the sky is the limit and this single factor, when it unfolds and is in place on a widespread scale, will cause the Chinese FX industry to absolutely mushroom in volume and power.

No wonder XTX Markets is running away with the largest number of top tier trades in the world. It clearly is the way to go.

Non-WikiFX

A trendy word which was coined by the skateboard-toting, latte drinking Millennial with dubious facial topiary has become a de facto term for certain websites that purport to have a central and distributed nature in their content and provision of information.

That word, Wiki, brought into the public domain by the brilliant Wikipedia, refers to user orientated content, therefore no bias or misinformation can be possible.

It has become a byword for trustworthiness of sources in a digital minefield.

The actual Oxford English Dictionary definition of Wiki is “a website or database developed collaboratively by a community of users, allowing any user to add and edit content.”

Benevolent indeed, so why do we tolerate sites that use the word Wiki, when they actually are far from that description in their operation?

This week, I was approached by several retail brokerages who alerted me to a practice which they say has been taking place at WikiFX, a website operated in South East Asia which allows retail traders to look up brokerages and see what are supposed to be impartial, user generated reviews.

One broker approached me and said “There is a new FX scam on the rise, this being the wikiFX website. They are blackmailing brokers. They post that a broker is not regulated and is a scam (when it is a regulated broker – Ed) and then call them and ask them to pay to remove that information.”

Another broker, albeit not one of the most reputable ones, actually went to task on this matter by stating on a public forum “WikiFX.com is spreading false information and false reviews. Their introduction video is quite entertaining, as it shows they are priding themselves in their “technology of prediction model of abnormity supervision” (yes you read that right!) or “model of supervision utility” (Google translate was apparently off that day!) to supposedly give accurate reviews.”

“Well that technology must not be working very well, as their reviews are based on anything but reality and actual research! This company is simply trying to come up by slandering the reputation of our company (and we’re pretty sure we’re not alone in this!).”

The broker continued “Almost 2 weeks ago, we came about this website that tagged us as “unregulated”. We contacted them to amend this false information they published about us and to date, not only was the information not corrected, we are now tagged as “suspicious clone” (who even knows what that means?!).”

“Despite our continued efforts to get to a resolution, they are now ignoring our emails. As a regulated company, we cannot allow so called professional review websites to spread lies about us! Criticism is always welcome, blatant lies are not!” he said.

I decided to follow this up, so I made a call to WikiFX to find out what their reasoning is, and if any of these allegations can be substantiated.

WikiFX’s Head of Business Development, based in Vietnam, told me “Firstly, I totally understand your feeling Sir. If I were you or your friend, i would be really upset.”

Friend? Interesting definition. I assume he means CEOs of regulated brokerages who approached me to alert the industry.

He continued, “Wikifx as a media, tries to provide traders around the world with all broker’s basic information including: licenses, where they are, how many year they have worked, software, trader’s complaints. On the other hand, I do believe that WikiFx wants to cooperate with all brokers, to make a win – win relationship.”

I had to straighten the spelling and grammar out, however you get the gist. Wanting to co-operate with brokers for what is often called ‘win win relationship’ in South East Asia contravenes the Wiki name that the site has, and certainly creating self-generated poor reviews and then asking an editorial team for money to remove them is not only extortion but certainly does not mean that this site gives impartial, user generated references about brokerages that can be taken at face value by traders.

WikiFX’s Head of Business Development continued “We have a guarantee plan for brokers in order to get the trader’s trust. It is not only a title, we definitely take responsible for traders if any things happen with broker that make trader can’t get money back” he said. How? That’s a mystery considering there is zero jurisdiction. Perhaps we could ask if they charge for this ‘service’ and then say we tried but cannot help.

Then came the gem. This individual began to resort to belittling. “Maybe your friend are misunderstand us, or our staff do not do their jobs well enough to explain clearly.”

Oh dear.

I further explained “There have been several people from brokers on public forums saying they’ve been asked to pay, or face having a bad review, and in one case, we have the conversation recorded.”

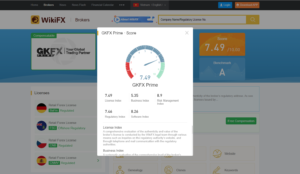

I was then shown how the system works, and that there is an index within which brokerages are given a score. That is actually a very good idea, if it is administered impartially, however the conversation led onto what I thought was coming next.

“As you can see, we have Risk management Index. In this example, GKFX use our services in the form of the guarantee plan to increase their Risk Management Index. So the score will get a bit higher.”

An answer to my original question was not forthcoming despite over five attempts during this conversation to receive a straight answer.

Of course, there are lots of retail sites around, especially in mainland China, which will ask for brokers to pay to remove fake reviews, or will attempt to damage their reputation unless a brown envelope changes hands, but they don’t purport to be UGC orientated ‘wiki’ sites.

Anyway, one can decide for oneself, just doing my bit here to ensure awareness. Mind how you go!

Wishing you all a great week ahead!